Bank lending to retail SMEs falls since Brexit – whilst large retailers see 20% rise

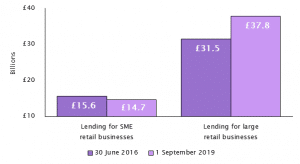

Bank lending to small and medium sized retailers in the UK has fallen 6% from £15.6bn* to £14.7bn since the Brexit vote in 2016, meanwhile large retailers have benefited from a sharp rise in bank lending, says accountants and business advisors, Moore.

Over the same period that lending to SME retailers has been tumbling lending to large retailers by banks has jumped by 20% from £31.5bn to £37.8bn.

Without additional finance, many retailers will struggle to trade through the tough times currently facing the industry.

Banks are becoming more risk averse and reluctant to lend due to Brexit related economic uncertainty. The figures suggest that some banks are favouring big businesses, who are typically seen as more able to repay any funds borrowed.

Moore says banks will have limits over what percentage of their loan book they will have concentrated in the retail sector. With big retailers increasing their borrowing so aggressively that means less finance for smaller retailers.

As well as needing finance to see them through the current volatile trading conditions, SME retailers also need to invest to ensure their stores and overall offering remain contemporary. Without that investment smaller retailers risk losing more ground to bigger competitors and to e-commerce.

Weak trading in the retail sector and a lack of finance has continued to push up insolvencies. There has been a 31% increase of insolvencies in the retail sector to 1,252 in the year to September 30 2019, up from 951 in the year prior to the Brexit vote. More funding may be needed so retailers can avoid falling victim to the insolvency trend.

Bridget Culverwell, director at Moore, says “It is a real worry for smaller retailers if banks are treating them less favourably than larger retailers.”

“With the final outcome of Brexit still uncertain, it is expected that banks will continue to be apprehensive to lend to the sector in the months ahead.”

“Small retailers are still big employers. They occupy space in high streets where larger retailers are not present and often not interested in being present. If too many small retailers fail then that leaves those parts of town centres with the highest level of vacant shops even emptier.”

Bank lending to small retailers falls 6%, whilst rising 20% for large retailers, since the Brexit vote

* Bank of England – September 30 2019