Coface Asia corporate payment survey 2021

Coface’s 2021 Asia Corporate Payment Survey, conducted between October 2020 and March 2021, provides insights into the evolution of payment behaviour and credit management practices of over 2,500 companies across the Asia Pacific region during a pandemic year. Respondents came from nine markets (Australia, China, Hong Kong SAR, India, Japan, Malaysia, Singapore, Thailand and Taiwan) and 13 sectors located in the Asia-Pacific region.

No deterioration of payment delays despite the impact of Covid

65% of respondents experienced payment delays in 2020, similar to 2019. Despite a weakened economic environment, the survey conducted by Coface shows that payment delays improved in 2020, with the average duration of overdue payments falling to a five-year low, thanks to strong government policy responses. Shorter payment delays were seen across six of the nine surveyed economies and 10 out of 13 sectors. This trend was partially due to robust and coordinated government policy responses to soften the impact of the pandemic on business activity, as well as the move by companies towards tightening credit management and strengthening cash-flow resiliency. This tighter credit policy was reflected by the average duration of payment delays in Asia Pacific, which fell to 79 days in 2020, down from 85 in 2019, and its shortest length since 2015.

However, there was a build-up of credit risks in Australia and Hong Kong, with both reporting a strong increase in late payments, and more crucially, a sharp rise in ultra-long payment delays (ULPDs, over 180 days) amounting to over 2% of annual turnover. According to Coface’s experience, 80% of ultra-long payment delays (ULPDs, over 180 days) are never paid. Meanwhile, the retail, construction, and transport sectors – among the worst hit by the pandemic – saw the largest increases in ULPDs over 2% of their annual turnover, indicating an increase in cash flow risk.

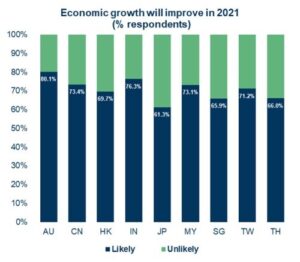

Economic improvement in 2021: Companies in Australia and the automotive industry are most optimistic

2020 was characterised by the shock of Covid-19 on both economies and society. Unlike previous recessions, which tended to be gradual and shallower, the pandemic recession was rapid and deep due to the unique elements of the coronavirus pandemic. Companies were surveyed about the impact of Covid-19 on their business operations. In Japan and Taiwan, a reduction in demand was the top reason impacting companies’ sales and cash-flows, whereas in China, higher material prices were the most-cited reason. In India, where many companies rely on migrant workers, the top impact cited was insufficient workforces due to lockdown measures disrupting business operations.

With robust and coordinated policy responses, an accelerated shift towards digitalisation, and countries reopening parts of their economy after strict lockdown measures, the recovery was quick but uneven. Companies nevertheless expect that economic growth will improve in 2021. Australian firms were the most optimistic, with 80% of respondents anticipating higher growth, followed by India (76%), China (73%), Malaysia (73%) and Taiwan (71%). In contrast, Japan was the only country where less than two-thirds of respondents (61%) expect an improvement in economic growth during 2021.

By sectors, automotive is the most confident regarding year-ahead sales, with 66% of respondents expecting an improvement. This was followed by energy (64%), metals (64%), paper (63%) and pharmaceutical (61%). The highest proportion of companies anticipating an improvement in cash flows over the next 12 months were found in automotive, agri-food, and pharmaceutical at 55% each, followed by metals (53%), paper (52%), and chemicals (51%).

Information & communications equipment export drives growth in Asia but risks remain

With the ongoing move towards “normal” business conditions, we expect the region to experience positive growth after contracting in 2020. The pace of expansion will be the fastest in India (+9.0%), which saw the sharpest contraction among the nine surveyed economies during 2020. This is followed by China (+7.5%), Singapore (+6.3%), Taiwan (+5.6%), Australia (5.0%), Hong Kong (+4.8%), Malaysia (+4.6%), Japan (+2.7%) and Thailand (+2.2%). External demand has been a key driver of the recovery for Asia, as a global shift towards remote working and remote learning drove a global need for information and communications (ICT) equipment.

This greatly benefited several economies in the region that are key exporters of ICT products , such as China (+40% YTD), Taiwan (21% YTD), Malaysia (28% YTD) and Singapore (9% YTD). An increase in capital investment also boosted sales of electronic and electrical machinery. However, the recovery in private consumption was much more gradual, and lagged behind growth in manufacturing and exports as labour market improvements remained weak and many parts of the APAC region experienced renewed mobility restrictions and lockdowns. Curbs on international travel remained largely in place, which prevented the tourism sector from mounting a recovery.

“Our baseline scenario assumes that there will be no new wave of Covid-19 infections in the second half of 2021, and that a ramp-up of vaccination improves the resiliency of the recovery. The caveat is that the current environment remains difficult to predict. Moreover, there are rising risks to the recovery, such as the global semiconductor shortage, which could limit Asian export growth, and rising commodity prices, which could compress corporate margins and weigh on demand,” explained Bernard Aw, Coface’s Asia-Pacific economist.

The complete report is available here.