FICO UK Credit Card Market Report: January 2023

New data from FICO on UK card trends appears to reflect the contrasting picture of the economy. January saw inflation slightly pegged back compared to the end of 2022; retail sales also improved marginally in the new year. In a similar vein, the FICO data shows that many of those consumers missing one credit card payment in December continued to struggle with their debts in the new year, with a marked increase in two missed payments. However, the balance for two missed payments dropped, potentially reflecting curtailed spending.

Highlights

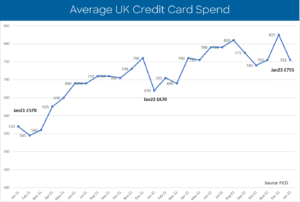

- Average total sales down 8% compared to December 2022 at £755

- Percentage of accounts with two missed payments 13.6% higher than December 2022

- Although average balance on accounts with two missed payments is 1.9% lower month-on-month

- Accounts missing one payment fall month-on-month by 0.7%

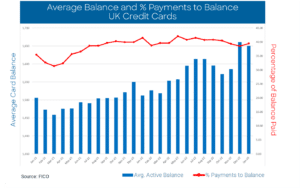

- Average balances across all accounts drop by 0.6% month-on-month to £1,650

FICO comment

Analysis of the largest consortium of UK cards data shows UK consumer credit behaviour in January 2023 generally following typical seasonal patterns. However, there was a spike in those customers missing two payments — 13.6% month on month — which could ring alarm bells for lenders.

December saw more accounts falling one month behind, and the increase in two missed payments in January appears to be moving the delinquency forwards. With Consumer Duty a priority for the FCA, lenders will want to ensure they are taking the right actions with those customers showing signs of financial difficulty. There may, however, be some comfort in the fact that the average balance of two missed payments continues to decrease and has been dropping since October 2022.

Lenders will also welcome the fact that the number of consumers missing one payment in January dropped month on month; usually in the first month of the new year there is an increase in one-month missed payments. However, this needs to be balanced against the fact that we saw a high increase in one-month missed payments in December, so this is more of a levelling off than a reduction and the percentage is still high. The percentage of payments to balance has also increased by 2.4% month-on-month after decreasing from September 2022.

With an increase usually seen in this behaviour post-Christmas this will be an interesting measure to track throughout the year as the cost of living crisis continues.

Key Trend Indicators – UK Cards January 2023

| Metric | Amount | Month-on-Month Change | Year-on-Year Change |

| Average UK Credit Card Spend | £755 | -8.1% | +13.2% |

| Average Card Balance | £1,650 | -0.6% | +9.1% |

| Percentage of Payments to Balance | 39.5% | +2.4% | -4.9% |

| Accounts with One Missed Payment | 1.7% | -0.7% | +9.1% |

| Accounts with Two Missed Payments | 0.36% | +13.6% | +20.8% |

| Accounts with Three Missed Payments | 0.20% | -4.2% | +21.1% |

| Average Credit Limit | £5,575 | +0.1% | +2.3% |

| Average Overlimit Spend | £90 | -1.1% | -24.8% |

| Cash Sales / Total Sales | 0.85% | +10.5% | -37.1% |

Source: FICO

The Data Charts

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers.