FICO UK Credit Card Market Report: June-August 2022

FICO’s report of UK card trends for summer 2022 (June-August) paints a picture of inconsistent consumer behaviour which will be challenging for lenders to manage as the cost-of-living crisis takes hold.

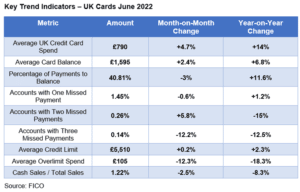

Highlights

- Average total sales were £790 in June and July and £810 in August – a more than 14% increase year on year for the three months

- The increase in the average balance for accounts with one and two missed payments continued in June and July, although it levelled out in August; this will still be a red flag for lenders

- Cash sales on credit cards increased by 6.7% in June and 3.4 percent in July – another worrying trend for lenders

FICO comment

Analysis of the largest consortium of UK cards data shows the percentage of consumers using their credit card to take out cash steadily increasing over the three months – a clear indicator of financial stress as the interest charged for cash on credit cards is always higher than standard purchases.

Total average sales on credit cards also increased across the summer. With media reports suggesting consumers have been reducing their spending in response to the cost-of-living crisis, this uplift in spend on credit cards illustrates the increasing reliance on credit rather than disposable income or savings. The average active balance on credit cards is now at its highest for over two years.

The percentage of payments to balance also reflects the pattern of inconsistency seen through the earlier months of the year. In June it dropped by 3% month on month; in July it increased by 1.7 percent and then in August it dropped again by 1.8%.

The percentage of missed payments also sends confusing messages for lenders. In June cardholders missing one payment remained almost static, but in July it increased by 2.2% and in August dropped by 4.6% compared to the previous month. However, the percentage of cardholders missing two or three payments increased steeply in August compared to July by 8.5% and 9.3% respectively.

This suggests that cardholders who miss more than one payment may not have the funds to catch up and are struggling with over indebtedness. There is also evidence that the percentage of cardholders spending over their credit limit has been slowly trending upwards since March. This could be another signal that some cardholders are over-indebted.

Lenders can use segmentation analysis on their portfolios to ensure that their web and mobile applications encourage consumers in distress to make contact at the first indications of difficulty, and to consider establishing special payment plans for those struggling to stay on top.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service produced by FICO® Advisors, the business consulting arm of FICO. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers.