Footfall still down on pre-pandemic levels

Covering the four weeks 01 August – 28 August 2021

2020 was a turbulent year in which much of retail bounced between being open and closed, impacting footfall significantly. To make meaningful comparisons to changes in footfall, all 2021 figures are compared with 2019 (pre-pandemic). This means our 2021 figures are now year-on-two-years (Yo2Y), rather than year-on-year (YoY).

According to BRC-Sensormatic IQ data:

- Total UK footfall decreased by 18.0% in August (Yo2Y), with a 10.0 percentage point increase from July. This is above the 3-month average decline of 24.6%.

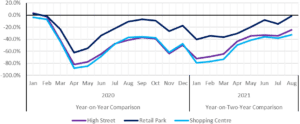

- Footfall on high streets declined by 24.8% in August (Yo2Y), 9.8 percentage points above last month’s rate and above the 3-month average decline of 31.0%.

- Retail parks saw footfall decrease by 1.6% (Yo2Y), 13.4 percentage points above last month’s rate and above the 3-month average decline of 10.0%.

- Shopping centre footfall declined by 32.9% (Yo2Y), 5.5 percentage points above last month’s rate and above the 3-month average decline of 36.6%.

- Wales saw the shallowest footfall decline of all regions at -16.5%, followed by Northern Ireland at -16.6% and England at -17.9%. Scotland saw the deepest decline at -21.2%.

Helen Dickinson OBE, chief-executive of British Retail Consortium, said: “Following months of little improvement, August footfall was a tentative step in the right direction. There were minor improvements with the return of some workers to the office and domestic tourism through August, however overall footfall remained significantly down compared to the pre-pandemic peak.

For our local communities to thrive, government must deliver on the commitment it made in the business rates review to reduce the overall burden of the tax, which is hindering retailers’ ability to invest and create jobs and is leading to store closures across the country. It is vital the government delivers on this commitment when it publishes the conclusion of its review over the coming months.”

Andy Sumpter, retail consultant EMEA for Sensormatic Solutions, commented: “Bolstered by staycationer shopper traffic and the Back To School boost, August saw footfall recovering to its highest point compared to pre-pandemic levels so far this year. In every UK city we track – including London, which has sorely felt the impact of slow returning commuter trade in recent months – showed improved shopper counts, as vaccine confidence won out against the fears and spread of the Delta variant.”

Sustaining this recovery into the Autumn – and as retailers head towards the critical Golden Quarter of peak trading – is no longer just reliant on maintaining consumer confidence. Getting stock on shelves has always been a given retail imperative. But amidst the ongoing disruption to stock availability, exacerbated by both Brexit and covid-19, shoring up supply chains to meet elevated levels of demand, and offering alternative delivery formats like click and collect to ease the burden on the digital fulfilment network, will become even more mission critical if recovery is set to continue.”

MONTHLY TOTAL UK RETAIL FOOTFALL (% CHANGE WITH 2019)

UK FOOTFALL BY LOCATION (% CHANGE WITH 2019)

TOTAL FOOTFALL BY REGION (% CHANGE WITH 2019)

| GROWTH RANK | REGION | % GROWTH Yo2Y |

| 1 | North West England | -10.8% |

| 2 | East Midlands | -13.3% |

| 3 | East of England | -13.8% |

| 4 | Yorkshire and the Humber | -13.8% |

| 5 | South West England | -13.9% |

| 6 | South East England | -16.1% |

| 7 | West Midlands | -16.2% |

| 8 | North East England | -16.2% |

| 9 | Wales | -16.5% |

| 10 | Northern Ireland | -16.6% |

| 11 | England | -17.9% |

| 12 | Scotland | -21.2% |

| 13 | London | -29.5% |

TOTAL FOOTFALL BY CITY (% CHANGE WITH 2019)

| GROWTH RANK | CITY | % GROWTH Yo2Y |

| 1 | Portsmouth | -9.9% |

| 2 | Manchester | -12.4% |

| 3 | Liverpool | -12.7% |

| 4 | Leeds | -13.3% |

| 5 | Cardiff | -14.3% |

| 6 | Nottingham | -15.1% |

| 7 | Bristol | -17.1% |

| 8 | Belfast | -19.1% |

| 9 | Glasgow | -20.3% |

| 10 | Birmingham | -27.9% |

| 11 | London | -28.6% |