Retail sales growth begins to slow

Now that we have passed the period from 2020 that was under strict lockdown conditions, this analysis will return to primarily reporting the sales results on a year-on-year basis. However, for certain measures a two-year comparison remains useful, which will be clearly signposted below.

Covering the four weeks 1 – 28 August 2021

- On a Total basis, sales increased by 3.0% in August, against a growth of 3.9% in the same month last year. This is below the 3-month average growth of 6.9% and the 12-month average growth of 10.3%.

- On a 2-year basis, Total retail sales grew 8.9% during August compared with the same month in 2019.

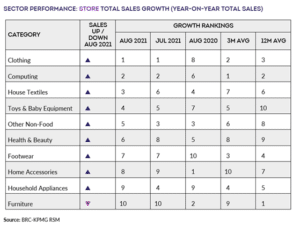

- Retailers reported a strong performance in Clothing, with increasing demand for formalwear, driven by the return to office working and social events.

- UK retail sales increased 1.5% on a Like-for-like basis from August 2020, when they had increased 4.7% from the preceding year. This is below the 3-month average growth of 4.5% the 12-month average growth of 10.9%.

- Over the three months to August, In-Store sales of Non-Food items grew 23.7% on a Total basis. This was slightly above the 12-month average growth of 21.7%. On a 2-year basis, stores saw a decline of 3.5% over the last three months.

- Over the three months to August, Food sales increased 2.9% on a Total basis and increased 1.9% on a Like-for-like basis. This is below the 12-month Total average growth of 5.4%. For the month of August, Food was in growth year-on-year.

- Over the three-months to August, Non-Food retail sales increased 10.3% on a Total basis and 6.8% on a like-for-like basis. This is below the 12-month Total average growth of 14.4%. For the month of August, Non-Food was in growth year-on-year.

- On a 2-year basis, Non-Food sales saw growth of 11.9% for the three-months to August.

- Online Non-Food sales decreased by 4.6% in August, against a growth of 42.4% in August 2020. This is below the 3-mth average decline of 3.5%.

- Non-Food Online penetration rate decreased to 38.3% this August from 42.0% in the same month last year. While down on last year, it was up 9.3 percentage points on the 29.0% seen at the same point in 2019.

Helen Dickinson OBE, chief executive | British Retail Consortium “As post-lockdown pent-up demand has softened, the growth in retail sales we have seen over the past few months slowed for August. Nonetheless, we still saw growth above pre-pandemic levels, as people returned to stores in greater numbers. With wedding season in full swing and workers gradually returning to the office, formalwear was a strong performer. Additionally, the bank holiday weekend and back-to-school buzz contributed to a rise in non-food sales. While the online sales growth has begun to slow, it is still high when compared with pre-pandemic growth rates. This demonstrates how the pandemic has shifted the digital-physical shopping balance and increased the linkage between the two channels.”

“With a precarious economic backdrop and retailers grappling with higher costs across the supply chain, the Government needs to deliver on its promise to reduce the burden of business rates that are holding back investment in recovery from the pandemic. If not, we will see the number of shuttered stores continue to rise and more jobs lost. This will seriously impact communities right across the country, and those already most economically deprived will be hit the hardest, putting the levelling up agenda in jeopardy.”

Don Williams, retail partner | KPMG “Much like the summer weather retail performance in August was mixed. Sales growth on the high street continued to slow, with footfall still below pre-pandemic levels and online sales took a retreat from the highs of last year, whilst some discretionary non-food categories continued their recovery.

“Overall, the high street saw 3% growth, dented by lower food sales growth of 1.9% as consumers enjoyed a fully re-opened hospitality sector. Online sales fell back by -2.5% compared to August 2020, though online penetration rates remained significantly above pre-pandemic levels, signalling the step up in online shopping is here to stay. Clothing, footwear and accessories continued their recovery with some healthy sales increases but from a much lower base, whilst technology and furniture/appliance categories suffered against very strong comparatives in 2020.

“With the retail recovery showing signs of slowing, the sector is expected to grow at a more muted rate as retailers face increasing challenges on a number of fronts. Inflation is expected to accelerate putting pressure on household spending, whilst retailers battle for share of wallet as consumers spend money on leisure, entertainment and travel. Staffing pressures remain and supply chain issues are being widely reported, with raw material shortages and challenges getting product into the UK and getting goods into customers‘ hands. This may feed into limited availability of certain products and the spectre of price rises remains.

“Retailers will be pinning their hopes on a more predictable normal with white collar workers returning to city centres in greater numbers from this month and a buoyant Christmas fuelled by some of the savings that consumers have made over the last 18 months of lockdown and restricted spending. Nonetheless, successful retailers will have to work very hard to ensure the right availability of the right product to satisfy the requirements of an ever more demanding customer.”

Food & Drink sector performance | Susan Barratt, CEO | IGD “Food and drink sales in August were broadly flat on 2020’s performance, with some spending switching from retail back into the out-of-home sector. Despite sales being limited by the dull weather, they were supported by staycations and the late summer Bank Holiday, which helped sales show a small amount of growth.

“IGD’s Shopper Confidence Index remained strong, continuing to hit one of the highest levels in the last five years. However, concern around inflation continues, with IGD’s ShopperVista revealing that 79% of shoppers expect food and grocery prices to get more expensive in the year ahead, up from 75% in July ’21. With much of the economy now open, more shoppers are changing what they spend their money on; some 73% have spent more on products and services in August, compared to 69% in June’21 and 31% are spending more on eating and drinking out, compared to 22% in June’21.”