Electric vehicle leasing: Is it a smart financial move?

Is leasing an electric vehicle worth it in the U.S.?

Is leasing an electric vehicle worth it in the U.S.?

Read this article to find out when EV leases make financial sense, when they don’t, and how savvy drivers can even turn buyouts into profit.

1. When electric vehicle leasing is a smart financial move in the US

Electric vehicle leasing wins when you don’t drive much and want predictability.

In this scenario, you basically get an inexpensive monthly payment, bundled insurance and maintenance, and no depreciation headache. For the average American driving 12,000 miles annually, this math is clean.

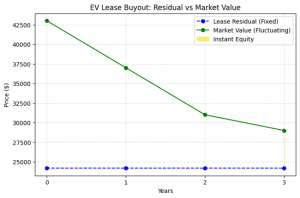

Take the 2026 Honda Prologue EX: New Jersey dealers are advertising a lease at $99/month with a buyout of $24,181.50 at lease-end. Meanwhile, used 2024 Prologues are trading around $35,000-$40,000 new.

If you lease that Prologue for three years, staying under 22,500 miles, you pay roughly $3,564 in total monthly payments plus $7,995 upfront, which is about $11,560 total. In other words, you get to drive a new car for $11,560, and at lease-end you can either walk away or end up keeping Honda after lease by buying it for $24,181, if market value supports it.

By the way, this works because Honda locked in that residual before used EV values crashed.

However, the real win happens with lease buyout arbitrage.

Because manufacturers set residual values years in advance, they often miss market shifts. EV depreciation has been brutal lately, so brands are artificially inflating incentives to move inventory. That creates a mismatch:

- Lease buyout price = based on old assumptions.

- Real market value = based on today’s reality.

As a result, you enjoy three years of the newest technology with no battery or depreciation worries.

2. When electric vehicle leasing isn’t a smart financial move in the US

Leasing starts to crumble the moment you drive more than 12,000 miles annually.

Standard EV leases allow 7,500–10,000 miles per year, with excess charges of 20–25 cents per mile. Drive 15,000 miles annually, and you’re looking at around $3,600–$4,500 worth of penalties over three years.

Suddenly, the “cheap monthly payment” advantage evaporates.

And mileage is tricky. You might think you’ll stay under 10,000 miles yearly—until year two brings a cross-country trip or a new job that doubles your commute. Now you’re underwater on the lease with no easy exit.

The second risk comes in the form of you actually liking the car.

The thing is, lease contracts are rigid. If the residual is $24,000 but the market value rises to $28,000, you can’t negotiate. You either pay the fixed buyout or walk away from a car you want to keep.

Oh, and that “zero depreciation” advantage? It vanishes if you plan to hold onto the vehicle long-term. Once you own it outright (through buyout or direct purchase), but EVs still lose significant value early.

For example, some popular EVs lose over 60% of their original value in five years:

- the Nissan LEAF loses about 64%,

- the Tesla Model S around 65%, and

- the Jaguar I‑PACE tops the list at 72%.

This shows that the steepest depreciation happens in the first few years, and the “protection” offered by a lease mostly applies to that early window.

In short? Leasing only shines if you want to trade every few years for the newest tech.

3. The lease buyout loophole: How to profit when manufacturers miscalculate

As we saw earlier, buying out a lease can sometimes create instant equity if market values exceed the residual. But the real edge comes from knowing how and when to spot these opportunities, not just assuming they exist.

As we saw earlier, buying out a lease can sometimes create instant equity if market values exceed the residual. But the real edge comes from knowing how and when to spot these opportunities, not just assuming they exist.

Lease buyout prices are fixed from day one, but EV markets are volatile. Some manufacturers overestimate value retention, while others underestimate it.

That mismatch opens short-lived windows for savvy drivers, so here’s where and what you should look for:

- Check three-year-old models of the same make and trim to compare actual market values against residuals before you sign a lease. Pay attention to shorter-term leases (24–36 months) and high-residual deals, as these often create the largest potential upside.

- Monitor incentives and regional market pricing. E.g., used EV prices can vary $2,000–$5,000 between states.

- Timing matters, too, so it is advisable that you start tracking values about 90 days before lease-end. Market swings can turn a profitable buyout into a loss quickly.

And consider resale options, as private sales often net more than dealer trade-ins, plus some buyers will pay a premium for low-mileage EVs with warranties remaining.

Extra leverage tip: Self-employed drivers can sometimes deduct buyout costs or claim depreciation if the car is used for business, adding another layer to the financial advantage.