Financial advisor Charlottesville VA: Secure future 2026

Building a resilient portfolio: A data-driven approach to wealth management

The core principles of a data-driven wealth management strategy

For many successful Virginia business owners and executives, the personal wealth we’ve built is deeply intertwined with our company’s performance. While this intense focus naturally drives growth, it can also inadvertently create uncertainty for our families’ long-term financial stability. The real challenge often lies in constructing a personal investment portfolio that is as resilient and thoughtfully designed as the businesses we’ve dedicated our lives to building.

For many successful Virginia business owners and executives, the personal wealth we’ve built is deeply intertwined with our company’s performance. While this intense focus naturally drives growth, it can also inadvertently create uncertainty for our families’ long-term financial stability. The real challenge often lies in constructing a personal investment portfolio that is as resilient and thoughtfully designed as the businesses we’ve dedicated our lives to building.

This crucial phase requires a deliberate shift in perspective: moving from the daily demands of running a company to strategically managing personal wealth for the decades ahead. How do we ensure our financial future is secure, diversified, and aligned with our deepest aspirations?

We will explore a data-driven approach to wealth management, outlining the core principles and practical steps that empower established professionals like us to build truly resilient portfolios. We aim to provide clarity on how to steer this transition, offering insights into effective strategies for long-term growth and capital preservation.

Many successful Virginia business owners and executives find that their personal wealth is deeply intertwined with their company’s performance. While this focus drives growth, it can also create uncertainty for your family’s long-term financial stability. The real challenge is building a personal portfolio that is as resilient and thoughtfully constructed as the business you’ve dedicated your life to. This requires a deliberate shift from running a company to managing personal wealth for the decades to come.

Who this article is for

This is for established business owners, partners, and senior executives in Virginia, particularly those in Charlottesville, Richmond, or Alexandria, who are beginning to think about the next chapter. It is for professionals whose personal net worth has grown significantly and now requires a more structured approach to management and preservation.

You may recognize these signals

- Your personal investment decisions feel reactive rather than strategic. We might find ourselves making choices based on headlines or anecdotes rather than a cohesive plan, leading to suboptimal outcomes.

- We worry that a market downturn could significantly delay our retirement. The thought of losing hard-earned capital can be paralyzing, especially when our personal wealth is concentrated in a few areas.

- We are unsure how to diversify away from the concentration of wealth in our business. Our business success often means a significant portion of our net worth is tied to its value, making broader diversification a complex but necessary task.

- We lack a clear plan for how our assets will generate income in retirement. Moving from active income generation to relying on passive income requires careful planning and a robust strategy.

Why this decision matters

A structured wealth management plan provides more than just financial returns; it provides stability and flexibility. It ensures our family is protected regardless of our business’s market cycle, creates a clear path toward retirement, and gives us the confidence to make important life decisions without financial hesitation. It is the foundation for a secure future, independent of the company we built. This proactive approach allows us to enjoy the fruits of our labor while safeguarding our financial legacy for future generations.

A sound strategy is not about chasing trends or timing the market. It is a disciplined, evidence-based process grounded in your specific circumstances. For business owners in the Roanoke Valley and across Virginia, this means building a framework that balances growth with capital preservation. This approach moves beyond speculation, focusing instead on a methodical path to financial security.

Principle 1: Aligning investments with life goals, not market hype

The most effective portfolios are designed to fund specific, tangible life goals—such as a planned retirement, a business transition, or a philanthropic legacy. Every investment decision should be weighed against its ability to help you achieve those outcomes within your defined timeline and risk tolerance. This approach shifts the focus from chasing short-term gains to building long-term reliability.

Financial advisors in Charlottesville, VA, typically offer a comprehensive suite of services designed to help clients align their investments with their life goals. These services often include:

- Financial planning: This foundational service involves creating a detailed roadmap for your financial future. It encompasses budgeting, cash flow analysis, and setting clear financial objectives.

- Wealth management: Beyond planning, it involves ongoing oversight and optimization of your entire financial picture, including investments, taxes, and estate planning.

- Retirement planning: A critical service for many, it focuses on ensuring you have sufficient assets to maintain your desired lifestyle in your non-working years. This includes strategies for accumulating wealth, creating income streams, and managing healthcare costs in retirement.

- Investment management: Advisors help construct and manage diversified portfolios custom to your risk profile and goals. This often involves selecting appropriate investment vehicles, such as stocks, bonds, mutual funds, and ETFs, and regularly rebalancing the portfolio.

- Estate planning: To ensure your legacy is protected and your wishes are carried out, advisors assist with wealth-transfer strategies, minimize estate taxes, and coordinate with legal professionals to establish wills and trusts.

For instance, when planning for retirement, an advisor won’t just look at investment returns. They’ll consider your desired retirement age, anticipated expenses, potential healthcare costs, and how your current investments fit into that picture. They can help you project how long your savings might last, providing peace of mind as you approach this significant life transition.

Principle 2: A fiduciary-first approach

Working with a fiduciary is fundamental. A fiduciary advisor is legally and ethically bound to act in your best interest, which eliminates many common conflicts of interest. This standard ensures that the advice you receive is exclusively focused on your financial well-being, not on generating commissions from product sales. This distinction is crucial for building trust and ensuring that your financial plan serves your objectives above all else.

Finding a fiduciary financial advisor in Charlottesville, VA, is straightforward, though it requires diligence. Here’s how:

- Ask directly: When interviewing potential advisors, explicitly ask if they operate under a fiduciary standard at all times. Some advisors may only act as fiduciaries in specific circumstances.

- Check credentials: Look for advisors with certifications like CERTIFIED FINANCIAL PLANNER™ (CFP®). While not all CFP® professionals are fiduciaries in every interaction, the CFP Board’s Code of Ethics and Standards of Conduct does require them to act as fiduciaries when providing financial advice. Other designations, such as Chartered Financial Analyst (CFA®), also imply a high ethical standard.

- Review form ADV: All registered investment advisors (RIAs) are required to file a Form ADV with the Securities and Exchange Commission (SEC) or state regulators. Part 2A of this form, known as the “brochure,” provides detailed information about the firm’s services, fees, disciplinary history, and whether they act as a fiduciary. You can typically find this on the SEC’s Investment Adviser Public Disclosure (IAPD) website.

- Understand compensation: Fiduciary advisors are often “fee-only,” meaning they are compensated solely by client fees (e.g., a percentage of assets under management, hourly rates, or flat fees). “Fee-based” advisors, on the other hand, can earn both client fees and commissions from product sales, which can introduce conflicts of interest. Understanding their compensation structure is key to identifying a true fiduciary.

The average fees or compensation structures for financial advisors in Charlottesville, VA, mirror national trends. Many advisors charge a percentage of assets under management (AUM), typically ranging from 0.5% to 1.5% annually, which often decreases as AUM increases. Other models include hourly fees (e.g., $150-$400 per hour), flat project-based fees for specific plans (e.g., $1,500-$7,500+), or retainers. Fee-only advisors are generally preferred for their transparent compensation and alignment with client interests.

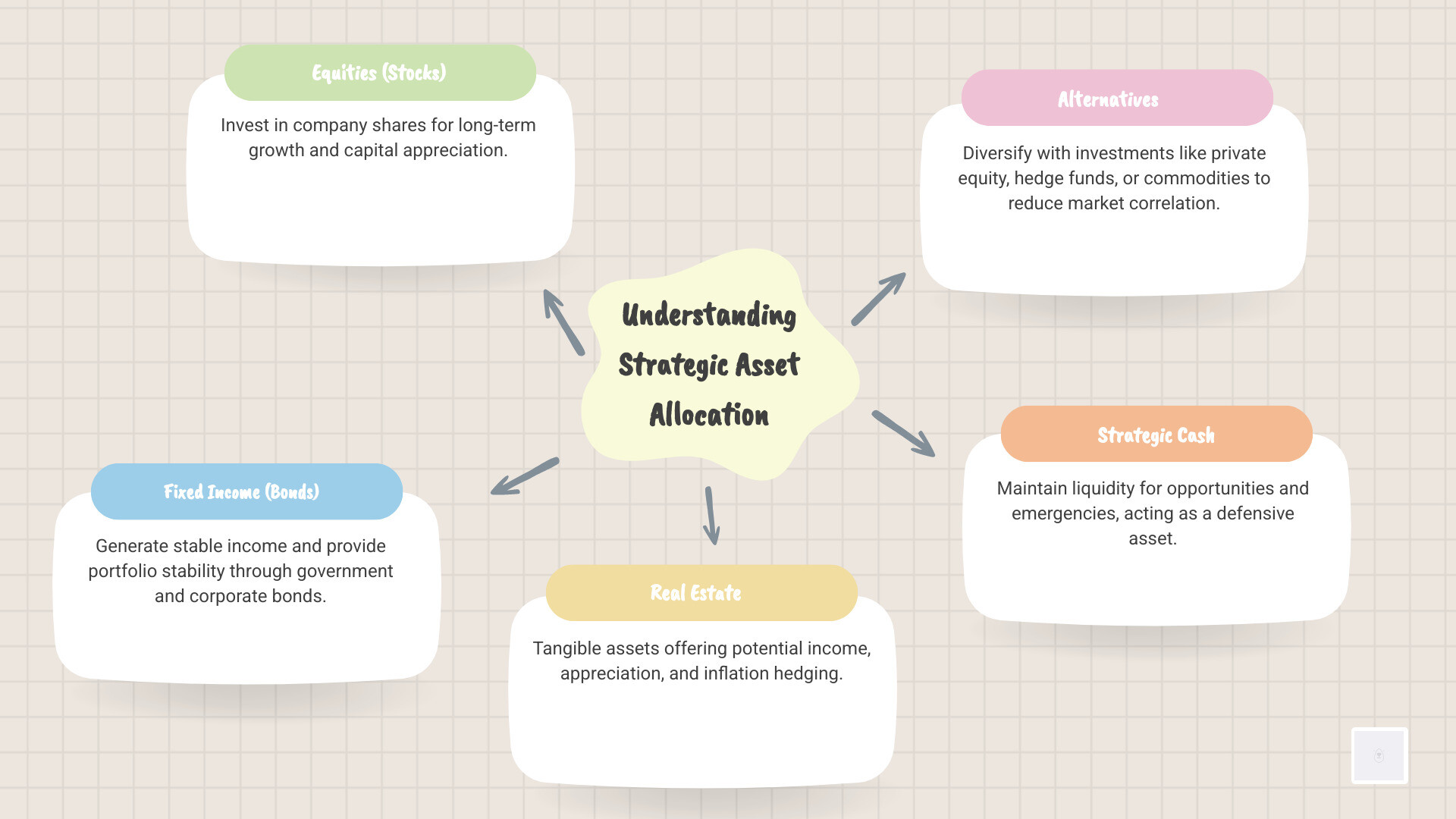

Principle 3: Comprehensive diversification

True diversification goes beyond a simple mix of stocks and bonds. It involves incorporating different asset classes, geographies, and investment styles that behave differently in various economic conditions. For many professionals, this also means strategically reducing the concentration of wealth tied up in a single business or real estate holding to build a more resilient financial base. This strategic approach to investment management and wealth planning helps mitigate risk and smooth out portfolio returns over the long term.

Financial advisors in Charlottesville, VA, help with investment management and wealth planning by:

- Assessing risk tolerance and goals: They start by understanding your individual risk appetite, financial objectives, and time horizon. This forms the foundation for all investment decisions.

- Developing an investment policy statement (IPS): This document outlines your investment goals, risk parameters, asset allocation targets, rebalancing rules, and other guidelines for managing your portfolio.

- Strategic asset allocation: Advisors determine the optimal mix of asset classes (e.g., equities, fixed income, real estate, alternatives) based on your IPS. This is a crucial step in managing risk and capturing returns.

- Investment selection: They research and select specific investment vehicles (e.g., individual stocks, bonds, mutual funds, ETFs) that align with your asset allocation strategy and overall financial plan.

- Portfolio monitoring and rebalancing: Advisors continuously monitor your portfolio’s performance and make adjustments as needed to ensure it stays aligned with your IPS. This includes rebalancing to maintain target asset allocations.

- Tax-efficient investing: They implement strategies to minimize taxes on investment gains, such as tax-loss harvesting, using tax-advantaged accounts (401(k)s, IRAs), and strategically allocating assets.

- Holistic wealth planning: Beyond investments, advisors integrate other elements of your financial life, including retirement planning, estate planning, insurance needs, and charitable giving, to create a cohesive wealth strategy. This ensures all components work together toward your ultimate financial goals.

For example, a firm might manage over $800 million in assets, indicating significant experience and scale in handling diverse client portfolios. Another firm, founded in 2000, has been providing continuous wealth management services for over two decades, demonstrating long-term stability and expertise in navigating various market cycles.

Practical steps for building your personal wealth management strategy

Translating principles into action requires a clear, methodical process. It begins with an honest assessment of where you are today and a clear vision for where you want to be. For many professionals in Virginia, the first step is a candid conversation with a Charlottesville wealth advisor to map out these considerations.

Evaluating and selecting the right advisor

Choosing a partner to manage your wealth is one of the most important financial decisions you will make. Look beyond marketing and focus on qualifications, compensation structure, and experience. A transparent advisor will welcome questions about their background and how they are paid.

Key factors to consider when choosing a financial advisor in Charlottesville, VA:

- Fiduciary standard: As discussed, ensure they are legally and ethically bound to act in your best interest at all times.

- Compensation structure: Understand how they are paid (fee-only, fee-based, commission-based) and how this aligns with your preferences and minimizes potential conflicts of interest.

- Credentials and certifications: Look for professionals with designations like CERTIFIED FINANCIAL PLANNER™ (CFP®), Chartered Financial Analyst (CFA®), Accredited Investment Fiduciary (AIF®), or Chartered Retirement Plans Specialist (CRPS®). These indicate specialized knowledge and a commitment to ethical practice.

- Experience and specialization: Consider their years of experience and whether they have expertise in areas relevant to your specific needs (e.g., business owner planning, retirement income, estate planning, multi-generational wealth). Some firms in Charlottesville specialize in serving business owners, pre-retirees, or families with complex financial needs.

- Client communication and relationship: Evaluate their communication style, responsiveness, and their plans for engaging with you. A strong client-advisor relationship is built on trust and clear communication.

- Services offered: Ensure the advisor provides the specific services you need, including comprehensive financial planning, investment management, tax planning, and estate planning coordination.

- Technology and tools: Inquire about the technology they use for planning, reporting, and client portals to improve your experience and transparency.

- Client testimonials and references: While not always publicly available, asking for references or looking for independent reviews can provide insight into other clients’ experiences.

To verify the background and experience of a financial advisor in Charlottesville, VA, several resources are available:

- FINRA BrokerCheck: This free online tool allows you to research the professional background of current and former FINRA-registered brokers and brokerage firms. It provides information on their licenses, employment history, and any disciplinary actions or customer complaints.

- SEC investment adviser public disclosure (IAPD): For investment advisors, the IAPD website provides access to their Form ADV filings, which detail their business practices, fees, services, and disciplinary history.

- CFP board website: If an advisor holds the CFP® designation, you can verify their certification status and any disciplinary history directly through the CFP Board’s website.

- Professional organizations: Websites for organizations such as the National Association of Personal Financial Advisors (NAPFA) or the Financial Planning Association (FPA) often include “find an advisor” tools that list members who adhere to specific ethical standards.

Developing your custom wealth management strategy

A generic plan is not a plan at all. Your strategy should be a documented roadmap that integrates investment management with tax planning, estate considerations, and retirement income needs. It should be a living document, reviewed regularly and adjusted as your life and goals evolve. This iterative process ensures your plan remains relevant and effective as your circumstances change.

This custom strategy often includes an Investment Policy Statement (IPS), which serves as the blueprint for your portfolio. It defines your investment objectives, risk tolerance, asset allocation, and guidelines for investment selection and monitoring. This document ensures consistency and discipline in your investment approach. Furthermore, it integrates tax planning strategies to minimize your tax burden and wealth transfer strategies to efficiently pass on your assets according to your wishes.

A framework for your first meeting

To ensure a productive conversation with a potential advisor, it helps to organize your thoughts.

- 1. Define your goals: What do you want your wealth to accomplish for you and your family? Be specific. Do you aim for early retirement, funding a grandchild’s education, leaving a philanthropic legacy, or selling your business?

- 2. Inventory your assets: Create a clear list of all your assets (investments, real estate, business equity, savings), liabilities (mortgages, loans), and income sources. This provides the advisor with a comprehensive picture of your current financial standing.

- 3. Assess your risk tolerance: How would you react to a significant market decline? Are you comfortable with aggressive growth strategies, or do you prioritize capital preservation? Understanding your psychological comfort with risk is vital for building a suitable portfolio.

- 4. Prepare your questions: Inquire about their philosophy, process, and how they serve clients like you. Ask about their experience with situations similar to yours, their communication frequency, and what a typical client relationship entails.

Frequently asked questions about wealth management

What are the different types of financial advisors available in Charlottesville, VA?

Charlottesville offers a diverse range of financial advisors. These generally fall into categories based on their compensation and services:

- Registered investment advisors (RIAs): These firms and their advisors are fiduciaries, legally bound to act in your best interest. They typically offer comprehensive financial planning and investment management.

- Broker-dealers: These firms primarily facilitate the buying and selling of securities. Advisors associated with broker-dealers may operate under a “suitability” standard, meaning recommendations must be suitable but not necessarily in your absolute best interest.

- Financial planners: While many advisors provide financial planning, some professionals focus solely on creating financial plans without managing investments.

- Specialized advisors: Some advisors or firms specialize in specific areas, such as retirement, estate, or tax planning, or in serving particular client demographics, such as business owners, medical professionals, or pre-retirees. For example, some firms have advisors who have been serving clients in the area since the early 2000s, demonstrating deep roots and specialized experience.

What is the difference between a “fee-only” and “fee-based” financial advisor?

A “fee-only” advisor is compensated solely by the fees paid directly by their clients, such as a percentage of assets under management (AUM), an hourly rate, or a flat planning fee. This structure is generally preferred because it minimizes potential conflicts of interest, as the advisor has no incentive to recommend specific products that pay them a commission.

A “fee-based” advisor can earn both client fees and commissions from selling financial products (like insurance policies or certain mutual funds). While they may act as fiduciaries in some aspects of their service, the commission component can create a conflict, incentivizing them to recommend products that benefit them financially rather than being solely in your best interest.

How does a wealth manager help with retirement planning specifically?

A wealth manager helps structure your portfolio to generate sustainable income throughout retirement. This includes creating a withdrawal strategy, managing investments to balance growth and safety, planning for potential healthcare costs, and optimizing for tax efficiency to ensure your savings last. They can also assist with consolidating various retirement funds, evaluating pension payouts, and determining the optimal time to claim Social Security benefits. The goal is to provide a clear path to a confident, secure retirement.

What credentials should I look for in a financial advisor?

Look for designations that require rigorous education, ethical standards, and experience. The CERTIFIED FINANCIAL PLANNER™ (CFP®) is a primary certification for comprehensive financial planning, indicating expertise in areas like retirement planning, investment management, tax planning, and estate planning. The Chartered Financial Analyst (CFA®) designation signifies deep expertise in investment analysis and portfolio management. Other valuable credentials include:

- AIF® (Accredited Investment Fiduciary®): Focuses on the fiduciary standard of care.

- CRPS® (Chartered Retirement Plans Specialist™): Specializes in retirement plans for businesses and individuals.

- EA (Enrolled Agent): Specializes in taxation and is authorized to represent taxpayers before the IRS.

- CTFA (Certified Trust and Fiduciary Advisor): Expertise in trusts, estates, and fiduciary responsibilities.

- AWMA® (Accredited Wealth Management Advisor®): Focuses on wealth management strategies for high-net-worth individuals.

These certifications demonstrate an advisor’s commitment to ongoing education and adherence to professional standards, providing an added layer of confidence in their expertise.

How often should I review my wealth management plan?

Your plan should be formally reviewed with your advisor at least annually, or whenever you experience a significant life event. Significant life events include the sale of a business, an inheritance, a change in marital status, the birth of a child or grandchild, a career change, or a major health event. These moments can significantly alter your financial landscape and require adjustments to your strategy to keep it aligned with your evolving goals and circumstances. Regular reviews help keep your financial roadmap current and effective.

Can a wealth manager help coordinate with my other professionals, like my CPA or attorney?

Yes, a key role of a wealth manager is to act as a “financial quarterback.” They should work collaboratively with your tax advisors (CPAs) and legal advisors (attorneys) to ensure your investment, tax, and estate plans are all aligned and working together efficiently. This integrated approach prevents potential conflicts, identifies missed opportunities, and ensures that all aspects of your financial life are cohesive and optimized toward your overarching goals. This coordination is particularly valuable for business owners with complex financial structures.

Gaining clarity and confidence

Building a resilient personal portfolio is a deliberate process that requires clarity, discipline, and expert guidance. By focusing on core principles and creating a strategy custom to your unique goals, you can achieve the financial independence and peace of mind necessary to enjoy the life you’ve worked so hard to build. The goal is not just to accumulate wealth, but to deploy it thoughtfully to support your family for generations to come.