Ultimate final expense insurance with no medical questions

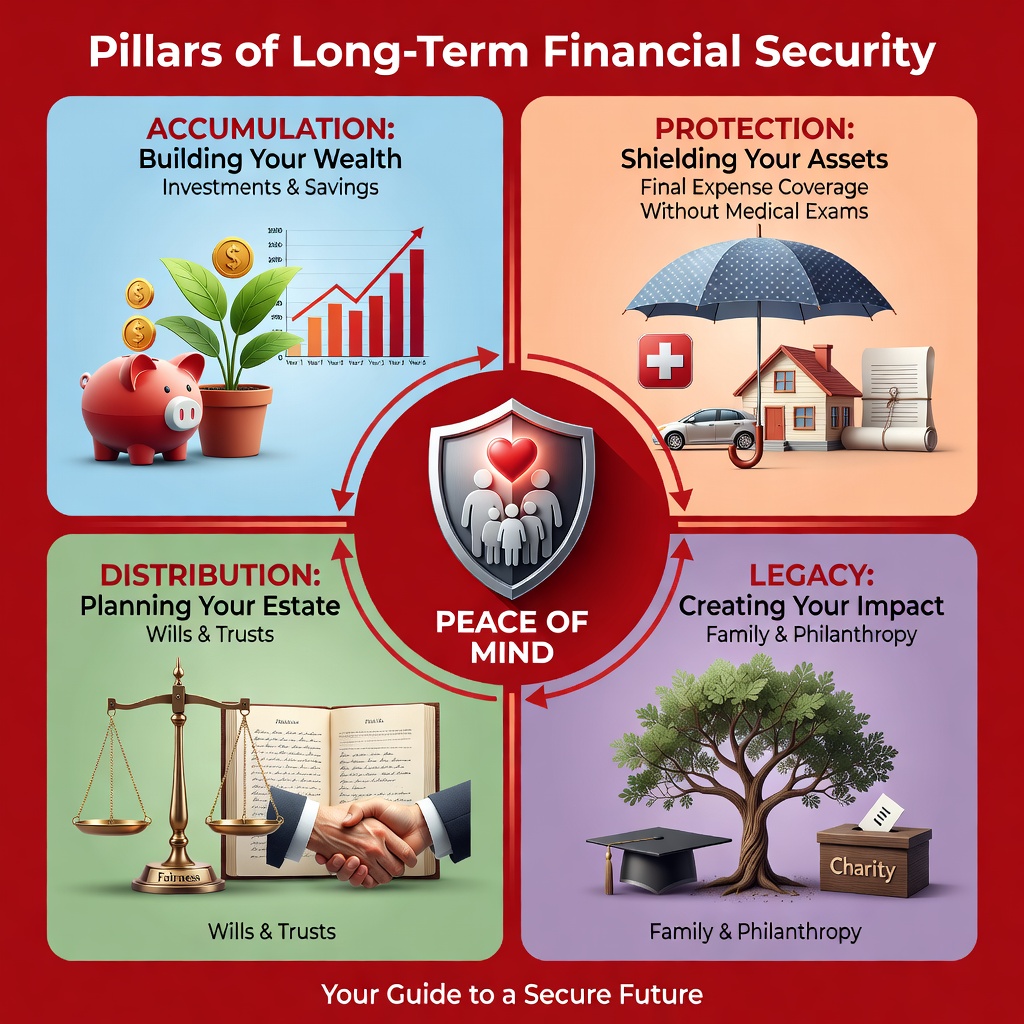

Long-term strategies for financial security and risk management

The role of financial planning and insurance in estate management

It’s natural to worry about the future. We want our financial decisions today to protect our loved ones tomorrow. We all aim to leave a legacy, not a burden.

It’s natural to worry about the future. We want our financial decisions today to protect our loved ones tomorrow. We all aim to leave a legacy, not a burden.

This is where smart financial planning and the right insurance become crucial. They offer peace of mind.

For many, making sure final expenses are covered is a top priority. This prevents financial strain on family. But what if health concerns make it hard to get traditional life insurance?

This is where final expense insurance with no medical questions offers a valuable solution. It provides coverage without the need for medical exams or lengthy health questionnaires.

This comprehensive guide will explore how this type of insurance fits into your long-term financial strategy. We will explain what it is and how it works. We will also show who benefits most, typical costs, and how it differs from other options.

Our goal is to help you understand how to secure peace of mind for both yourself and your family.

Effective financial planning extends far beyond accumulating wealth; it encompasses the strategic management and protection of your estate for future generations. A well-constructed financial plan, particularly one that integrates appropriate insurance solutions, is fundamental to ensuring your wishes are honored and your loved ones are cared for without undue financial stress.

One of the primary objectives of estate management is asset protection. This means safeguarding your accumulated wealth—your home, savings, investments—from being prematurely depleted by unforeseen costs. Without adequate provisions, significant expenses such as end-of-life care or funeral arrangements could necessitate liquidating assets, potentially at an inopportune time, reducing the inheritance intended for your beneficiaries.

Tax efficiency is another critical component. Life insurance proceeds, for instance, are generally received income tax-free by beneficiaries, providing a substantial lump sum that can be used to cover estate taxes, outstanding debts, or simply provide financial support. This tax-advantaged payout ensures that more of your legacy reaches your family, rather than being diminished by tax obligations.

Liquidity is often overlooked but incredibly important. Upon a person’s passing, their estate can sometimes take months or even years to settle, especially if it goes through probate. During this period, beneficiaries may face immediate financial needs, such as funeral costs, legal fees, or ongoing living expenses, without immediate access to the estate’s assets. Life insurance provides quick liquidity, delivering a death benefit directly to named beneficiaries, bypassing the often-lengthy probate process and ensuring funds are available when they are most needed.

Regularly reviewing your financial and insurance coverage is also vital. Research indicates that fewer than 40 per cent of Canadians revisit their coverage each year. This oversight can lead to outdated policies that no longer align with current life circumstances, financial goals, or the rising costs of living and dying. We encourage periodic evaluations of your policies to ensure they remain relevant and effective.

Finally, strategic beneficiary designations are key to probate avoidance. By naming specific beneficiaries on your insurance policies and retirement accounts, these assets can often be transferred directly to them outside of the probate court system, saving time, legal fees, and maintaining privacy. This proactive step is a cornerstone of efficient estate management.

Understanding final expense insurance with no medical questions

Final expense insurance, often referred to as “burial insurance” or “funeral insurance,” is a specific type of whole life insurance designed to cover end-of-life costs. What sets it apart, and what makes it particularly valuable for many individuals, is the “no medical questions” aspect. This means that obtaining coverage does not require a medical exam or an extensive health questionnaire, simplifying the application process significantly.

This type of policy typically falls into one of two categories:

- Simplified issue: While it doesn’t require a medical exam, it does involve answering a few basic health questions. Approval is generally fast, and coverage can be issued quickly.

- Guaranteed acceptance: This is the most accessible form, as it requires no medical exam and no health questions whatsoever. Acceptance is guaranteed, making it an ideal option for those with significant health challenges who may not qualify for other types of life insurance.

Both simplified issue and guaranteed acceptance policies offer permanent coverage, meaning the policy remains in force for your entire life, as long as premiums are paid. This contrasts with term life insurance, which only covers you for a specific period. With final expense insurance, your beneficiaries are guaranteed to receive a death benefit upon your passing, providing invaluable financial support.

A key feature of these policies is their fixed premiums. Once your policy is in force, your premium payments will remain the same for the life of the policy, making budgeting predictable, especially for those on a fixed income. Furthermore, final expense policies often build cash value over time. This cash value can be accessed through policy loans or withdrawals, offering a potential source of funds during your lifetime, though accessing it will reduce the death benefit.

The primary purpose of final expense insurance is to provide immediate liquidity to your loved ones. The death benefit is paid directly to your designated beneficiaries, who can then use the funds for any purpose, including:

- Funeral and burial costs

- Cremation expenses

- Outstanding medical bills

- Legal and probate fees

- Unpaid debts (credit cards, personal loans)

- Travel expenses for family members attending the service

This ensures that your family can focus on grieving and honoring your memory, rather than scrambling to cover unexpected costs. For those seeking accessible coverage without the hurdles of medical underwriting, exploring options like Lunsford no-exam final expense can provide a clear path to securing this essential protection.

To better understand how final expense insurance compares to other life insurance options, consider the following table:

Feature Final Expense (Whole Life, Simplified/Guaranteed Issue) Term Life Insurance Medical Exam No medical exam or limited health questions Often required, comprehensive health questionnaire Coverage Type Permanent (lasts your entire life) Temporary (lasts for a specific term, e.g., 10, 20, 30 years) Premiums Fixed; generally remain level for life Fixed for the term; increase upon renewal Cash Value Builds cash value over time No cash value Purpose Cover final expenses, small debts, leave a small legacy Income replacement, large debt coverage (mortgage) Coverage Amount Typically $3,000 – $40,000 Can be significantly higher, e.g., $100,000 – $1,000,000+ Eligibility High approval rate, even with health issues Health-dependent; can be difficult to obtain with significant health issues Eligibility and Coverage Limits for No-Exam Policies

Final expense insurance with no medical questions is specifically designed to be accessible, particularly for individuals who might find it challenging to qualify for traditional life insurance due to age or health conditions. We often see that the eligibility age ranges for these policies typically span from 50 to 85 years old, though some providers may offer coverage starting as young as 20 or extending slightly beyond 85. The core principle is guaranteed approval or highly simplified underwriting, making it a viable option for a broad spectrum of seniors.

A significant advantage is that your health history does not typically prevent you from obtaining coverage. Whether you have pre-existing conditions like diabetes, heart disease, or have experienced a stroke, these policies are structured to provide coverage without a detailed medical review. This accessibility is crucial for peace of mind, ensuring that health challenges don’t become a barrier to protecting your family from end-of-life costs.

The coverage amounts available for final expense insurance generally range from $3,000 to $40,000. While these amounts are lower than those typically found in traditional life insurance, they are specifically tailored to cover the immediate costs associated with funerals, burials, and other final expenses. Many providers offer options up to $25,000 or $35,000, which is often sufficient to alleviate the financial burden on surviving family members.

These policies are particularly beneficial for individuals on a fixed income, as the fixed premiums allow for predictable budgeting. The ability to secure coverage regardless of health status means that financial planning for final expenses doesn’t have to be a luxury reserved for the perfectly healthy. It becomes an accessible tool for everyone.

The importance of this financial safety net cannot be overstated. The unexpected loss of a loved one, particularly a spouse, can have a devastating financial impact. For example, statistics show that widows under 55 saw an average after-tax family income drop by more than $15,000 in a year, and the share living in low-income households nearly tripled. While final expense insurance is typically for older adults, this statistic highlights the broader financial vulnerability that can arise from a death, underscoring the need for any form of financial protection for survivors.

Beyond the basic death benefit, some final expense policies may offer optional policy riders. These can include features like an accidental death benefit, which pays out an enhanced amount if death is due to an accident, or a terminal illness rider, allowing access to a portion of the death benefit while still living if diagnosed with a qualifying condition. These riders can further customize the policy to meet specific needs and provide additional layers of protection.

Cost factors and strategic risk management

When considering final expense insurance with no medical questions, understanding how premiums are determined and the inherent risk management features of these policies is crucial. The primary premium determinants include your age at the time of application, your gender, your smoking status, and the specific coverage amount you choose. Generally, the younger and healthier you are (even if no medical exam is required, smoking status is often considered), the lower your premiums will be.

It’s important to recognize that because these policies offer guaranteed acceptance or simplified underwriting, they inherently carry a higher risk for the insurance provider compared to fully underwritten policies. This increased risk is often managed through specific policy structures, such as graded death benefits. A graded death benefit means that if the policyholder passes away from natural causes within the first two years (the “waiting period”) of the policy, the beneficiaries typically receive a refund of the premiums paid, often with a small amount of interest (e.g., 10% or 110% of premiums), rather than the full death benefit. However, if death occurs due to an accident during this initial period, the full death benefit is usually paid out immediately. After the two-year waiting period, the full death benefit is paid for death from any cause. This waiting period is a standard feature that allows insurers to offer coverage to individuals regardless of their health history.

The financial implications of end-of-life costs are substantial. For instance, The cost of dying in Canada can range from $5,000 to $10,000+, with cremation costs up to $5,000 and burial plots exceeding $25,000 in some cities. In the United States, data from the National Funeral Directors Association indicates that the national median cost of a funeral with a viewing and burial in 2023 was approximately $8,300, while a funeral with cremation was about $6,280. These figures underscore the significant financial burden that final expenses can place on grieving families, highlighting the critical role of final expense insurance.

Many policies also offer an enhanced accidental death coverage, where if death is due to an accident, the payout could be 3 to 5 times the face amount of the policy. This provides an additional layer of protection against sudden and unforeseen circumstances.

While the premiums for no-medical-question policies can be higher than for traditional, fully underwritten life insurance (due to the lack of medical screening), they offer an invaluable solution for those who might otherwise be uninsurable. The fixed premiums and guaranteed coverage provide a predictable and secure way to plan for future expenses, effectively mitigating the financial risk your passing could pose to your loved ones.

Practical steps for implementation and claims

Securing final expense insurance with no medical questions is designed to be a straightforward process, reflecting its purpose of providing accessible coverage. The application process is typically much simpler than for traditional life insurance. Often, it involves completing a short, one-page form either online or with the assistance of an agent. For guaranteed acceptance policies, there are usually no health questions at all, making approval virtually certain within the eligible age range. For simplified issue policies, you might answer a few basic health questions, but no medical exam or blood work is required. This ease of application means you can often get coverage approved and in force very quickly.

Understanding the potential costs your family might face is a crucial step in determining your coverage needs. As we’ve noted, the average funeral costs more than $9,000 today, a figure that can easily burden loved ones already grappling with grief. Many people mistakenly believe that government benefits will cover these costs. However, the Social Security Administration, for example, provides only a one-time death payment of $255 to a surviving spouse or child, which is a fraction of the actual expenses. This stark difference highlights the necessity of having dedicated final expense coverage.

When the time comes to file a claim, the process is also designed to be as simple as possible for your beneficiaries. Typically, they will need to:

- Notify the insurer: Contact the insurance company as soon as possible after your passing.

- Provide a death certificate: This is the primary document required to verify the death.

- Complete a claim form: The insurer will provide a form for the beneficiary to fill out.

Once these steps are completed, the beneficiary payouts are usually processed quickly, often within a few days to a couple of weeks. This swift payout is a significant advantage, as it provides immediate funds for your family to cover funeral costs, settle any outstanding debt settlement, or take care of lingering medical bill coverage without having to wait for probate or other estate settlements. The flexibility of the lump-sum death benefit means your beneficiaries can use the money for whatever they deem most necessary, providing true financial relief during a difficult time.

Frequently asked questions about financial planning and insurance

We understand that navigating financial planning and insurance options can bring up many questions, especially when considering sensitive topics like end-of-life arrangements. Here, we address some common inquiries to provide further clarity.

How does financial planning and insurance address funeral costs?

Financial planning, particularly through dedicated final expense insurance, directly addresses funeral costs by providing a predetermined lump-sum payout to your beneficiaries. With the national median cost of a funeral with a viewing and burial around $8,300, and cremation around $6,280, these expenses can be substantial. Final expense policies are designed to cover these costs, preventing your family from having to dip into savings, take out loans, or make difficult financial decisions during a time of grief. The lump sum is paid quickly, offering immediate relief and ensuring that your final wishes can be honored without financial strain. Moreover, by locking in coverage now, you can help protect against future inflation, ensuring the benefit remains relevant to rising costs.

Why is financial planning and insurance vital for seniors with health issues?

For seniors with health issues, final expense insurance with no medical questions is particularly vital because it offers guaranteed acceptance or simplified underwriting. This means that unlike traditional life insurance, you won’t be denied coverage due to pre-existing conditions like heart disease, diabetes, or a history of cancer. The absence of medical exams and lengthy health questionnaires removes significant barriers, making it accessible to a demographic often excluded from other insurance products. Some providers even report that 99% of applicants qualify, ensuring that nearly everyone can secure permanent protection for their loved ones. This provides immense peace of mind, knowing that your health status won’t prevent you from providing for your family’s future financial needs.

What are the limitations of no-medical question policies?

While final expense insurance with no medical questions offers significant advantages in accessibility, it’s important to be aware of certain limitations:

- Graded benefits: Most guaranteed acceptance policies include a two-year waiting period for natural death. If you pass away from natural causes within this period, your beneficiaries typically receive a refund of the premiums paid, often with a small amount of interest, rather than the full death benefit. However, accidental death is usually covered immediately.

- Premium costs: Because insurers take on more risk by not requiring medical exams, the premium costs for no-medical-question policies can be higher compared to fully underwritten policies offering similar coverage amounts.

- Lower coverage caps: The lower coverage caps, typically ranging from $3,000 to $40,000, mean these policies are designed for final expenses and not for income replacement or large estate planning needs. If you require substantial coverage, a fully underwritten policy might be more suitable if you qualify.

- Interest-only refunds: During the graded benefit period, beneficiaries receive a refund of premiums, not the full death benefit, for non-accidental deaths. This is a crucial distinction to understand.

Despite these limitations, for many individuals, particularly seniors or those with health concerns, the benefits of guaranteed access to coverage and predictable premiums often outweigh these considerations.

Conclusion

In the journey of life, securing your financial future and protecting your loved ones remains a paramount concern. Final expense insurance with no medical questions stands out as a compassionate and practical solution within a comprehensive long-term financial strategy. It offers the invaluable gift of peace of mind, ensuring that your passing does not become a financial burden for those you cherish most.

By providing a direct, tax-free death benefit, these policies enable you to build a lasting legacy, not just of memories, but of financial responsibility and care. They empower you with financial autonomy, allowing you to plan for your final wishes on your terms, regardless of health status. This commitment to long-term stability and family protection is fundamental to sound financial planning.

We encourage you to explore how final expense insurance can integrate into your overall financial plan, providing a clear path to securing your family’s future and ensuring your peace of mind.