SMEs warned over hidden borrowing costs as rate hike fears grow amid Middle East tensions

Fears of rising borrowing costs are intensifying as escalating tensions involving Iran ripple through global markets, prompting expectations that the Bank of England could keep interest rates higher for longer.

As businesses brace for increased financing costs, global financial services firm Ebury highlights that headline rates may only tell part of the story for SMEs navigating an already complex lending environment.

For internationally active SMEs, borrowing costs are not captured by headline interest rates alone. They are determined by how capital is accessed, how frequently it is used, and the conditions attached when requirements change.

Finance leaders typically understand base interest and fees, but contingent costs are less visible.

Non-utilisation fees on committed facilities reduce the cost advantage of undrawn liquidity. Early repayment charges and make-whole clauses limit flexibility and can reduce cash flow efficiency. Legal, documentation and amendment fees also accumulate over time and are often disconnected from actual credit usage.

These costs are not always reflected in initial pricing discussions, but they materially impact the total cost of capital.

Cross-border activity adds further complexity. Borrowing in one currency while paying suppliers in another introduces FX exposure that can outweigh interest costs. Where currency flexibility is restricted, financing structures can influence operational decisions. The ability to draw, repay and settle in multiple currencies is therefore as material as pricing for internationally active businesses.

Market data1 indicates SMEs often overestimate interest costs and underestimate ancillary charges. While American Express analysis shows fees and penalties can significantly increase total borrowing costs, particularly for revolving or short-term credit. This can result in underutilised facilities or delayed repayment decisions that reduce balance sheet efficiency.

The most reliable test is simple – if capital is used briefly or repaid early, does the cost adjust accordingly, if not, the borrowing model is misaligned.

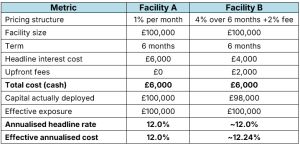

For example, an uncommitted, unsecured facility priced at 1% per month over six months equates to a 12% annualised cost on £100,000, or £6,000 in total interest. By comparison, a facility priced at 4% over the same period plus a 2% structuring fee produces a similar headline cost.

However, the 2% fee is paid upfront, meaning £100,000 of interest-bearing exposure is incurred against £98,000 of deployed capital. On an annualised basis, the effective cost increases to approximately 12.24%. The headline rate is lower, but the effective cost is higher.

Charles Hardaker, global head of lending at international financial services firm Ebury, said: “Ultimately, the true cost of borrowing is defined not by the headline rate, but by how capital behaves in practice. Fees on unused liquidity, penalties on early repayment, and currency constraints all shape real financing outcomes. “For internationally active SMEs, flexibility and transparency matter as much as price. In a period of geopolitical uncertainty driving rate volatility, businesses cannot rely on headline pricing as a true guide to affordability.

“Finance leaders should be scrutinising total cost under real usage scenarios, not theoretical ones, and ensuring their funding structures remain resilient in volatile markets. Efficient capital is not just a cost issue, but a strategic advantage when conditions shift quickly.”