Britain loses 6,000 storefronts in five years

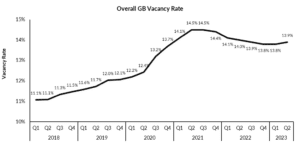

- In Q2 2023, the overall GB vacancy rate increased to 13.9%, which was a 0.1 percentage point worse than Q1. It was a 0.1 percentage point better than the same period last year.

- Shopping Centre vacancies remain unchanged at 17.8%, the same level as Q1.

- High Street vacancies increased to 13.9% in Q2, 0.1% worse than Q1.

- Retail Park vacancies fell to 8.1% in Q2, a 0.6 percentage point improvement from Q1 2023. It continues to remain the retail location with by far the lowest vacancy rate.

- Geographically, Greater London, Southeast and East of England again had the lowest vacancy rates. The highest rates were in the Northeast, followed by Wales and Scotland.

Helen Dickinson OBE, chief executive of the British Retail Consortium, said: “The past five years saw Britain lose 6,000 retail outlets, with crippling business rates and the impact of the Covid lockdowns a key part of decisions to close stores and think twice about new openings. The North and Midlands continue to see the highest amount of empty storefronts. London’s vacancy rate remains the lowest, improving over the last quarter thanks to the opening of new flagship stores, more office workers, and tourists visiting the capital.”

“To inject more vibrancy into high streets and town centres, and prevent further store closures, government should review the broken business rates system. Currently, there’s an additional £400m going on retailers’ bills next April, which will put a brake on the vital investment that our towns and cities so desperately need. The government announcement earlier in the week about making changes of use to vacant units easier is welcome but it’s important local councils have a cohesive plan, and don’t leave gap-toothed high streets that are no longer a customer destination and risk becoming inviable. Government should go one step further and freeze rates bills next year. ”

Lucy Stainton, commercial director, Local Data Company, said: “The headline findings from Q2 are unlikely to have come as a surprise to anyone, with economic pressure from rising interest rates and inflation already mounting as the year began. Current challenges to businesses have been compounded by tightening discretionary spend and a dip in confidence among consumers. The economic headwinds that have made the headlines have filtered into the data, reflected in a slight rise in the overall vacancy rate.

“The high street has seen some of the most notable impacts, with rising rents and increased competition putting pressure on small and independent businesses, who may struggle to meet high operating costs. Across all location types, vacancy has reached critical levels, highlighting an ever-increasing need to redevelop units to breathe life back into retail destinations.

“Retail is a diverse industry; each retail and leisure subsector faces its own unique challenges, but also, importantly, has its own unique strengths. As the only location type to see a decrease in long-term vacancy (more than three years) this quarter, retail parks continue to prove resilient, bolstered by their strong occupancy fundamentals and relatively small lot sizes. Retail parks have shown us excellent examples of agile strategy in action, splitting larger units into smaller ones or converting space for alternative uses to successfully revitalise vacant stock. The current climate is undeniably difficult, but it should not be overlooked that today’s retailers are more innovative and future-thinking than ever.

“With the continuing trend in mind, we do not foresee any improvements to vacancy rate in future. However, given that the latest rises in vacancy have not been particularly significant, we anticipate that any increases in the near future will be gradual.”

| Current | 1 Quarter Ago | 1 Year Ago | ||

| Rank | Q2 2023 | Q1 2023 | Q2 2022 | |

| 1 | Greater London | 10.8% | 11.1% | 11.1% |

| 2 | South East | 11.4% | 11.3% | 11.7% |

| 3 | East of England | 13.0% | 12.8% | 13.1% |

| 4 | South West | 13.4% | 13.5% | 13.7% |

| 5 | East Midlands | 14.8% | 14.5% | 15.0% |

| 6 | Yorkshire and the Humber | 14.9% | 14.9% | 15.4% |

| 7 | North West | 15.3% | 15.2% | 15.4% |

| 8 | West Midlands | 15.9% | 15.8% | 15.7% |

| 9 | Scotland | 15.9% | 15.7% | 15.7% |

| 10 | Wales | 17.0% | 16.5% | 16.7% |

| 11 | North East | 17.5% | 17.5% | 18.8% |