FICO UK Credit Card Market Report: July 2024

The FICO UK Credit Card Market Report for July 2024 reveals a month-on-month drop in spending, reflecting the same trend seen in 2023. However, risk managers will need to be alert to the increase in customers missing payments, with established customers (those who have had their credit card for 1-5 years) having the highest percentage of missed payments.

Highlights

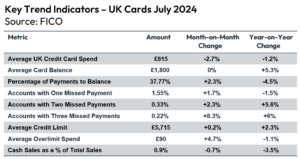

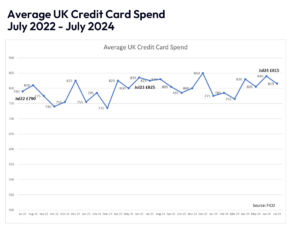

- Spending on credit cards dropped by 2.7% month-on-month and 1.2% year-on-year, to £815

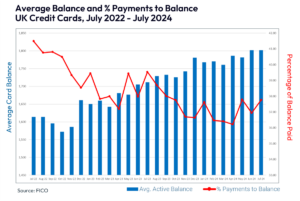

- July saw a 2.3% month-on-month increase in the percentage of balances paid, to 37.8%

- The number of customers missing payments across one, two and three months increased in July; a 2.3% increase for two missed payments was particularly surprising after the 6.5% drop in June for those missing one payment

- The average balance for consumers missing one payment increased by 0.3% on the previous month and 4.4% in 2023; the average balance for customers missing two payments decreased by 0.3% month-on-month but remains 4.7% higher than the previous year

- In July, 3.46% of customers took out cash on their card, equating to a 0.5% increase in the previous month but an annual drop of 4.8%

FICO Comment

While spend dropped by 2.7% month-on-month in July, to an average of £815, it will be interesting to see how consumers manage their credit commitments and spending in the coming months, potentially influenced by the August interest rate cut, as well as the predicted higher utility bills on their way. The effect of inflation also continues to be evident, with average balances 5.3% higher than 2023.

Of potential concern for risk managers will be the fluctuating pattern of missed payments. With the number of customers missing payments increasing month-on-month across all cycles and steadily trending up over the last two years, issuers should consider pre-collections treatments such as sending out payment reminders, offering more flexible payment options and utilising more customer preferred communication methods, supported by self-service channels.

Established customers (who have held their credit card for between one and five years) have the highest percentage of missed payments. Many customers in this group will have taken out cards during the pandemic, when their affordability may have been inflated due to lack of spending opportunities. They may also have taken on promotional offers such as balance transfers; as these offers expire, they may now be struggling to pay off higher APRs.

In line with Consumer Duty, financial institutions should review affordability metrics for customers coming to the end of promotional offers and move them onto rates more suited to their affordability profile, rather than taking a “one size fits all” approach.

The average balances for customers missing one, two and three payments have been trending up over the last two years. However, the overall average credit card balance has also been increasing and the ratio of delinquent balance to overall balance remains flat, indicating that balances for those customers missing payments is not increasing at a faster rate than for the overall balance.

Cash usage tends to increase over the summer months and this pattern is evident for July with 3.5% of customers taking out cash on their card, equating to a 0.5% increase month-on-month. The monthly increase is, however, smaller than increases seen in the last two years, and July’s usage was 4.8% lower year-on-year. With cash usage on cards a potential indicator of financial stress, it will be important to monitor if the upwards trajectory continues into September, as it has in previous years.