FICO UK credit card market report: June 2023

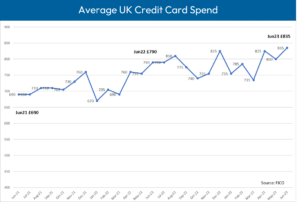

The latest FICO data on UK credit card trends reflects the impact of inflation on consumers’ budgets, as average spend hit its highest point in the 17 years since FICO records began, and average balances continued to track upwards.

Although inflation started to drop in June 2023, the FICO report reveals the longer-term impact of rising costs over the last 12 months. The data suggests that savings are starting to come under pressure, as the percentage of payments to balance dropped by 3.7% in June and the number of customers missing 2 payments is 26.6% higher than June 2022.

The percentage of accounts going over their limit has also shown a marked increase over the last 12 months, with new accounts (those open less than 12 months) showing the sharpest increase.

Highlights

- Average spend increased 4.8% month-on-month to £835, the highest level since 2006 (when FICO reporting began)

- The percentage of payments to balance dropped by 3.7% to 38% in June

- The average balance continues to trend upwards at £1,705 in June – a 1.7% increase month-on-month and 6.9% year-on-year

- The pattern of missed payments continued to be erratic, with customers missing one payment in June decreasing by 6.6%

- Accounts rolling forwards from one to two missed payments continued to increase steadily – 7.6% higher in June than May and 26.6% higher year-on-year

- The percentage of accounts going over their limit has also tracked consistently upwards over the last 12 months – increasing by 51% since March 2022

- Another indicator of financial stress is the use of credit cards to take out cash – with the latest FICO data showing that 3.6% of customers used their credit cards to withdraw cash in June, increasing 5.7% month-on-month and 7.5% year-on-year

FICO comment

The latest FICO data illustrates the continuing balancing act between high living costs and disposable income and savings. Whilst average spend has increased to the highest level since FICO reporting began in 2006, the up-and-down pattern of missed payments and the balance on those accounts missing payments suggest that savings are continuing to play their part. With two and three missed payment volumes trending upwards, the average missed payment balance is also increasing for these two groups since January and February 2023 respectively, although year on year they are still lower. The average balance for accounts with one missed payment has increased by 11% since June 2021.

However, because higher average balances overall correlate with higher missed payment balances, FICO has also reviewed the one, two and three missed payment balance compared to the overall current balance. In all three cases, in the last few months this ratio has been flat, indicating that missed payment balances are not increasing at a faster rate than the overall current balance. This also suggests that issuers have robust risk management strategies in place, and are giving limit increase offers to customers who are not going to subsequently miss payments, and are making effective pre-delinquent and overlimit accept / decline decisions.

Another key factor for lenders is the repayment behaviour of established customers who have had their credit card for between one and five years. These cardholders continue to have the highest percentage of missed payments, which is likely to be impacted by introductory rates such as balance transfer offers ending. Lenders will need to proactively support this group in the months leading up to these rates coming to an end, with the new Consumer Duty Guidelines expecting issuers to ensure vulnerable customers are on the right product.

Key Trend Indicators – UK Cards June 2023

Source: FICO

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers.