FICO UK credit card market report: June 2024

The FICO UK Credit Card Market Report for June 2024 reflects the usual seasonal uplift in consumer spending over the summer months. However, the data also suggests that consumers are managing their credit debt effectively. Whilst May 2024 saw quite significant month-on-month increases in late payments, lenders will be encouraged by the fact these have not carried over into June to the same extent. One area of concern is the increasing trend in balances for customers missing three payments.

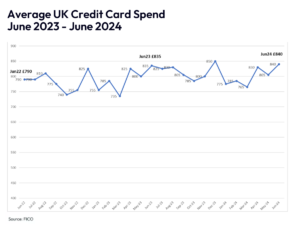

Highlights

- Credit card spending rose 4.2% from May to June 2024, now standing at an average of £840 and 0.1% higher than June 2023

- In line with usual seasonal trends, average balances increased by 1.1% in June to £1,800; this is 5.7% higher than June 2023

- The percentage of balance paid dropped by 2.3% month-on-month in June to 36.9%, reflecting the increase in spend and overall balance. It is also 2.7% lower year-on-year, although the pattern of lower payments to balance seen in the early part of 2024 has steadied

- After rising quite significantly from April to May (8.3%), the number of cardholders who missed one payment fell by 6.5% from May to June

- The average balance for cardholders missing one payment has remained higher year-on-year for two years, and was £2,235 in June

- Although there was an increase in May in the number of customers missing one payment, this has not rolled into seeing higher numbers in June missing two payments. In fact, for the second month in a row there has been a decrease in customers missing two payments.

- June also saw a significant drop in customers missing three payments; however, this is still 2% higher year-on-year

- The use of credit cards to take out cash has continued to increase, following the typical summer trend. At 3.45%, it is 3.4% higher month-on-month

FICO Comment

Traditionally the summer months see consumer spending increase and the FICO data, which reflects activity across the majority of UK consumer credit card providers, underlines this. However, it is just 0.1% higher year-on-year, which is considerably lower than current inflation figures, and does seem to suggest an overall caution amongst consumers.

The recent Barclays data which showed the first drop in spending by their cardholders for three years, also suggests a lack of consumer confidence during the pre-election period. Regardless, as spending increases over the summer months, it is likely that payments to balance will fall, leading to higher average balances and requiring further vigilance from lenders.

A positive approach by cardholders to credit debt management is reflected in the fact that the marked increase in one missed payments seen in May has not rolled over into two missed payments in June. However, vigilance is necessary for the cardholders with longer-term debt, with those missing three payments rising 2% year-on-year. Average balances for three missed payments now stand at £3,050, which is 7% higher than the same time last year, and this will be of considerable concern to lenders.

The use of credit cards to withdraw cash is another important signal of consumer financial management. Whilst in June this rose by 3.4% compared to May, it is 3.7% lower year-on-year.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers. For more information on these trends, contact FICO.

Please click on this link to download the press release