FICO UK Credit Card Market Report: October 2022

FICO’s latest report of UK card trends — for October 2022 — illustrates the push and pull of personal finances as consumers attempt to manage existing credit commitments while facing an increased cost of living.

Highlights

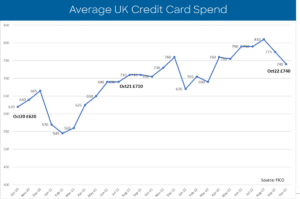

- Average total sales were 5% lower than September at £740

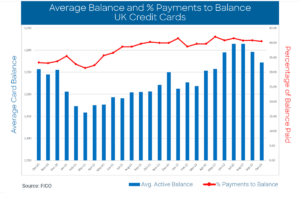

- The average active balance on credit card accounts also dropped in October to £1,570 – 1.5% lower than September

- The percentage of payments to balance dropped by 0.8% in October, continuing a trend seen since May

- Year-on-year missed payments have increased across all payment cycles, with two missed payments showing the greatest year on year growth at nearly 7%

- Those missing one payment in September struggled to stay on top of their debt as a 7% month-on-month increase in two missed payments recorded

- But consumers reduced reliance on credit cards for cash withdrawals with a 5.5% drop month-on-month

FICO comment

Analysis of the largest consortium of UK cards data illustrates the financial challenges faced by many people, as pandemic savings dwindle and the cost-of-living escalates. While the latest ONS data reports a small 0.5% rebound in GDP for the month, in the three months to October GDP shrank by 0.3% compared with the previous three months. This drop in spending is also reflected in the FICO data.

Average spend across credit card accounts dropped by £70 over September and October. And the percentage of payments to balance – reflecting both earnings and savings to stay on top of credit commitments – dropped by 0.8% month-on-month.

But perhaps most significant for credit providers is the year-on-year trend in missed payments. Across all payment cycles – one, two and three missed payments – there has been an increase over October 2021.

With two missed payments increasing month on month by 6.8% in October, credit providers will be wanting to understand the causes to offer the right support to account holders.

There is, however, one area where financial prudence is evident. The percentage of accountholders using their card to withdraw cash dropped month-on-month by 5.5% in October and, reflecting a pattern seen all year, by 22.3% year-on-year. It appears that cardholders are aware of the high cost of using credit cards to withdraw cash due to the higher APR charged.

Lenders can use segmentation analysis on their portfolios to ensure that their web and mobile applications encourage consumers in distress to make contact at the first indications of difficulty, and to consider establishing special payment plans for those struggling to stay on top.

The Data Charts

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers.