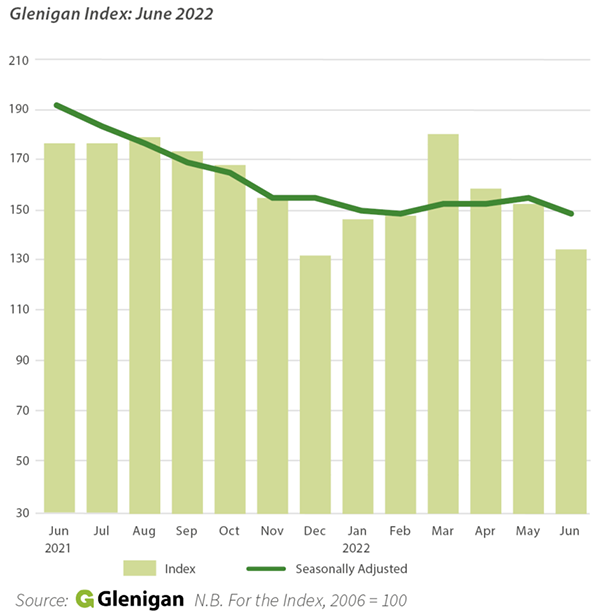

Glenigan index of construction starts to end of June 2022

- The value of underlying work starting on-site during Q2 2022 fell 5% against the preceding three months to stand 27% lower than a year ago.

- While residential project-starts increased 17% against the preceding three-month period, the value remained 21% down on the previous year.

- Non-residential construction-starts fell by more than a fifth (-22%) compared with Q1 and declined 29% against the previous year.

- Infrastructure project-starts performed particularly poorly in Q2, falling 27% against the preceding three months to stand 47% lower than a year ago.

Commenting on the latest numbers Rhys Gadsby, senior economist at Glenigan said: “Project-starts returned to decline in June as construction material inflation, currently riding at 25% year-on-year, continues to disrupt industry activity. While strong growth in private housing-starts may provide the industry with some positivity, declines among the civil engineering and non-residential sectors are largely holding back any form of recovery.”

Sector analysis

Residential project-starts improved during Q2 with the value rising 17% against the preceding quarter. However, the value remained 21% down on the previous year. Private housing work starting on-site advanced strongly (+43%) compared with Q1 levels, buoyed potentially by developers initiating work ahead of new building regulations. Despite this, private housing work starting on-site fell 14% against the previous year. Social housing project-starts performed poorly having slipped back 42% against the preceding quarter and previous year.

Performance among the non-residential sectors was largely negative. Only retail achieved growth against the preceding quarter (+6%) despite project-starts still remaining 28% lower than a year ago. Community & amenity-starts fell 1% against the preceding quarter but increased 21% against the previous year.

While health construction-starts remained unchanged on the preceding quarter, the value fell by a quarter compared with a year ago. Industrial project-starts also fell by a quarter against the previous year, but also experienced the greatest fall (-36%) against the preceding quarter of any non-residential sector. Hotel & Leisure (-32%), Offices (-23%) and Education (-21%) also experienced strong declines during Q2 to stand 40%, 30% and 37% lower than a year ago respectively.

Civil engineering experienced a very poor period for project-starts with the value having experienced the greatest declines against both the preceding quarter (-27%) and previous year (-47%). Utilities suffered the weakest period, with project-starts falling 30% during Q2 to stand almost half (-48%) the value of the previous year. This was the strongest decline of any sector against the previous year. Similarly, infrastructure-starts fell by a quarter against the preceding quarter and 46% compared with a year ago.

Regional Outlook

Performance among UK regions was very mixed in Q2. On a positive note, the most-northern regions of England performed well with growth of 7% in the North East and 2% in the North West against the preceding quarter.

While project-starts were up 2% against the previous year in the North West, the value fell 2% in the North East. Northern Ireland also experienced a strong period, with growth of 3% against the preceding quarter and 44% compared with a year ago.

The South West (+11%) also experienced an increase during Q2 but project-starts remained a third lower than the previous year. Construction-starts in the East Midlands remained unchanged against the preceding quarter but experienced the greatest decline (-47%) against the previous year.

Two areas performed particularly poorly, one being London which experienced a 30% fall against the preceding three months to stand 45% lower than a year ago. The other was Yorkshire & the Humber, which suffered the heaviest decline against the preceding quarter (-32%) and a 43% fall against the previous year.

| Glenigan Index | Residential | Non-Residential | Civil Engineering | |||||

| Month | Index | % change y-o-y | Index | % change y-o-y | Index | % change y-o-y | Index | % change y-o-y |

| Jun-21 | 179.1 | 74% | 246 | 87% | 129 | 72% | 190 | 40% |

| Jul-21 | 179.0 | 60% | 241 | 63% | 137 | 63% | 168 | 39% |

| Aug-21 | 181.4 | 39% | 256 | 42% | 141 | 42% | 127 | 12% |

| Sep-21 | 176.0 | 25% | 245 | 21% | 139 | 39% | 125 | -5% |

| Oct-21 | 169.5 | 6% | 238 | 4% | 133 | 20% | 119 | -28% |

| Nov-21 | 156.4 | -6% | 208 | -16% | 123 | 15% | 140 | -18% |

| Dec-21 | 133.6 | -4% | 186 | -11% | 101 | 9% | 117 | -12% |

| Jan-22 | 148.4 | -7% | 192 | -23% | 122 | 24% | 127 | -13% |

| Feb-22 | 149.5 | -11% | 187 | -27% | 132 | 25% | 111 | -32% |

| Mar-22 | 182.8 | -13% | 227 | -31% | 158 | 21% | 154 | -17% |

| Apr-22 | 160.7 | -17% | 204 | -31% | 132 | 7% | 152 | -18% |

| May-22 | 153.1 | -21% | 201 | -29% | 117 | -9% | 162 | -14% |

| Jun-22 | 130.8 | -27% | 195 | -21% | 91 | -29% | 102 | -47% |