London office space trends 2025: What the latest data tells us about price and availability

London’s office market has continued to evolve throughout 2025 as it has done for many years.

While hybrid work continues to redefine how companies use space, office rents in prime areas have surged – even as vacancy rates across the city hit record highs.

In this guide, we’ll explore all of the latest data on the London Office scene, brought to us by London Office Space.

Prime rents continue to rise

Rents for the prime space in London continue to rise (no surprise there):

- In Mayfair and St. James’s, headline rents now exceed £150 per sq ft, with some deals hitting £200 per sq ft – a record high for London.

- In the City of London, Grade A offices are commanding up to £100–£110 per sq ft, particularly in new trophy towers.

- By contrast, more affordable submarkets like Docklands remain in the £40–£60 per sq ft range, while Shoreditch and City Fringe areas average around £50–£70 per sq ft.

According to londonofficespace.com data, rent growth has been strongest in the City and Southbank, with year-on-year gains of up to 17%. This is driven by high competition for modern, ESG-compliant buildings.

The “flight to quality” is splitting the market

Not all buildings are benefitting equally from rising rents. The market is increasingly defined by a “flight to quality”:

- Grade A offices with strong sustainability credentials (like BREEAM or EPC A ratings) are seeing high demand and low vacancy.

- Older buildings with outdated layouts or inefficient systems are struggling to attract tenants – even at discounted rates.

One in-depth analysis from londonofficespace.com revealed that over 50% of leasing activity in 2024 was for sustainable, high-spec buildings. Companies are prioritising comfort, energy performance, and amenities over size alone.

This dynamic is leading to rental premiums for well-located, future-proof buildings – while landlords with legacy stock face pressure to refurbish or reposition.

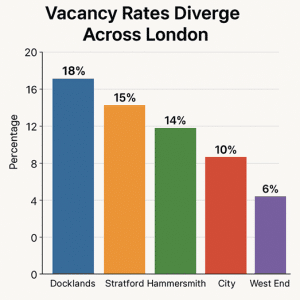

Vacancy rates hit 20-year highs – but not everywhere

Despite the boom in prime rents, vacancy rates across London reached their highest levels in two decades in late 2024. LondonOfficeSpace.com reports:

Despite the boom in prime rents, vacancy rates across London reached their highest levels in two decades in late 2024. LondonOfficeSpace.com reports:

- City-wide office vacancy sits around 10%, up from 5% pre-pandemic.

- Docklands and Canary Wharf have some of the highest levels, with 15–18% of space currently vacant.

- Hammersmith and Stratford have also seen vacancies climb.

- In contrast, the West End remains tight, with vacancy near 6–7%.

This split reflects the current supply-demand imbalance: while central Grade A space is in short supply, large volumes of older stock are going unused.

Limited new supply is holding up prices

You might expect record vacancy to drive prices down – but that hasn’t happened across the board.

Why?

Because new office construction in London is still well below historical averages. According to market analysts:

- Around 15.8 million sq ft of office space was under construction in 2024 – slightly less than in 2023.

- Only 3.9 million sq ft is expected to complete in 2025, with much of it already pre-let.

- Roughly 42% of upcoming space for 2025 was already committed by tenants before completion.Demand is changing

Office use has changed significantly in the last 5 years, and with this change comes a change in demand.

Here’s what LondonOfficeSpace.com has observed in the past year:

- Companies are leasing less space, and focusing on higher quality offices with smaller footprints.

- Shorter leases are more popular than ever – who knows what the future holds?

- Collaborative layouts, breakout zones, and wellness facilities are now “must-haves” for hybrid teams.

Interestingly, mid-2024 saw a record number of deals for sub-10,000 sq ft units, especially among tech, finance, and professional services firms.

Who’s driving demand in 2025?

The top three sectors behind office take-up in London remain consistent, per latest reports:

- Finance and insurance – roughly one-third of total leasing activity.

- Professional services – law firms, consultants, and accountancy firms.

- Tech and media – particularly AI, fintech, and creative startups.

In Q1 2025, major moves included large financial firms consolidating into newly built towers in the City, while several tech firms downsized but retained central space in Shoreditch and Clerkenwell.

Serviced office and coworking providers have also begun expanding again to meet rising demand for flexible, ready-to-use offices – particularly in the West End and fringe markets.

The West End: London’s strongest submarket

If one area deserves special mention, it’s the West End. From Soho to Mayfair, the market has rebounded faster and stronger than nearly anywhere else in the UK:

- Rents are at all-time highs, with premiums driven by limited availability.

- Vacancy remains the lowest in the capital, hovering below 7%.

- Mid-week occupancy is back to pre-pandemic levels in many buildings, as businesses increase office attendance.

This has made the West End highly competitive for occupiers – and increasingly attractive to investors.

Canary Wharf and Docklands: A market in transition

At the other end of the spectrum, Canary Wharf and the wider Docklands area are facing challenges.

- Vacancy rates exceed 15%, driven by several large occupiers exiting the area.

- Major banks like HSBC and Clifford Chance announced plans to relocate to the City by 2026.

- Landlords are responding with redevelopment plans and repurposing schemes, including mixed-use retail and residential conversions.

The outlook is mixed: while Docklands still offers value, its dominance as a financial hub is fading, with tenants now seeking more central or flexible options.

What’s next for London’s office market?

Looking ahead, the market is likely to remain polarised but active:

- Prime rents will continue to rise in high-demand areas, driven by limited supply and strong ESG expectations.

- Vacancy rates may slowly decline as legacy space is refurbished, repurposed, or converted to residential.

- Tenants will keep prioritising flexibility, quality, and location over square footage.

To stay in the game, expect landlords to focus on supporting hybrid working patterns and sustainability.

Wrapping it up

The London office market in 2025 is no longer about “back to normal.” It’s about new expectations, new priorities, and a rebalancing of the city’s commercial core.

Whether you’re a business looking to relocate or an investor eyeing emerging trends, the message is clear: location still matters – but quality now matters more.

For the latest listings and submarket breakdowns, visit londonofficespace.com.