The manufacturing cash flow gap: Why profit isn’t cash

A manufacturer can be busy, profitable on paper, and still unable to make payroll on Friday. It’s one of the cruellest facts of running a product business: a full order book doesn’t pay wages, and a healthy margin doesn’t help if the cash arrives three months after the bills do. For the many small manufacturers that make up the bulk of the sector, this gap between spending and being paid is the single biggest threat to survival — bigger, often, than competition or demand. Understanding it is the first step to financing around it.

A manufacturer can be busy, profitable on paper, and still unable to make payroll on Friday. It’s one of the cruellest facts of running a product business: a full order book doesn’t pay wages, and a healthy margin doesn’t help if the cash arrives three months after the bills do. For the many small manufacturers that make up the bulk of the sector, this gap between spending and being paid is the single biggest threat to survival — bigger, often, than competition or demand. Understanding it is the first step to financing around it.

The manufacturing cash flow gap is the timing mismatch between when a business pays to make something and when it gets paid for selling it. Materials, machine time, and labour are paid for upfront; customers settle their invoices weeks or months later. The result is a stretch where the work is done, the profit is real on paper, but the bank balance is empty.

Why profit and cash are not the same thing

The timing mismatch

Profit is an accounting idea: revenue minus costs over a period. Cash is what’s actually in the account on any given day. A business can record a profit on an order the moment it ships, while the money for that order won’t land for another 60 or 90 days. In between, the firm still has to buy the next batch of materials, run the machines, and pay its people. Profit says the business is winning; cash flow decides whether it survives long enough to enjoy it.

Why manufacturing feels it worse

Service businesses spend mostly on people and can scale costs up and down. Manufacturers carry a heavier, earlier burden: raw materials bought in lot sizes, tooling, energy, and production labour, all paid before a finished unit exists. Most manufacturers are small — the overwhelming majority of firms in the sector employ fewer than 100 people — so they carry that front-loaded cost with thin reserves and limited room to absorb a late payment. A single slow-paying customer can stall the whole operation.

Anatomy of the gap

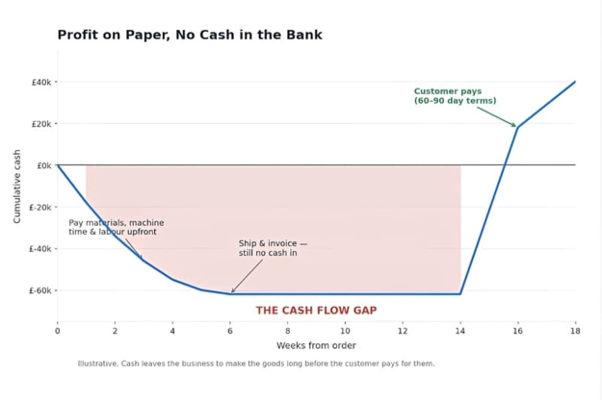

The gap has a shape, and it’s worth seeing clearly. Cash goes out at the start of a job and comes back at the end, and the distance between those two points is where businesses get into trouble.

Money out first

Production spends money before it earns any. The business has already paid for raw materials, machine time, and labour by the time a part is finished. A product company might pay an outsourced parts manufacturer for a full production run upfront, or put down a sizeable deposit, long before a single unit reaches a customer. Add freight, duty, and storage, and a large order can mean a large cash outflow weeks or months ahead of any revenue.

Money in last

Then comes the wait. Trade customers and retailers commonly pay on 30, 60, or 90-day terms, and often later in practice than on paper. The bigger and more creditworthy the customer, the longer the terms they tend to demand. So the supplier funds the entire production cycle — and a chunk of the customer’s working capital too — out of its own pocket until the invoice finally clears.

| Stage of the cycle | Cash effect | Typical timing |

| Buy materials, book machine time | Cash out | Day 0 |

| Production and labour | Cash out | Weeks 1–6 |

| Ship and invoice | No cash yet | Week 6 |

| Customer pays | Cash in | Week 14–18 |

When growth makes it worse

When growth makes it worse

Here’s the part that catches good businesses out: winning a big order can be more dangerous than losing one. A larger order means a larger upfront spend on materials and production, but the payment still arrives on the same delayed terms — only now the sum at risk is bigger. A business growing quickly can run out of cash precisely because it’s succeeding, buying ever more stock and production ahead of receipts it hasn’t collected yet. Picture a small firm that lands a contract twice its usual size: it must fund double the materials and machine time now, but the larger customer pays on 90-day terms, so the very win that should fund growth instead drains the account for a full quarter. The accountants call it overtrading. The owner just calls it terrifying.

The finance that bridges the gap

This is where commercial finance earns its place. None of these tools fix a broken business, but they smooth the timing so a sound one doesn’t trip over its own success. Each works against a different part of the cycle.

Against your invoices

Invoice finance and factoring advance most of an invoice’s value as soon as it’s raised, rather than making the supplier wait the full term. The receivable becomes cash within days, and the lender is repaid when the customer settles. For a business whose pain is slow-paying customers, it targets the problem directly.

Against your assets

Asset-based lending borrows against what the business already owns — receivables, equipment, and inventory together — to release a revolving line of working capital. Asset finance does the same for the machines themselves, spreading the cost of equipment over its working life instead of draining cash in one hit.

Against the order

Production and purchase-order finance fund the costs of fulfilling a specific order, with repayment tied to the eventual sale, so the facility settles itself once the buyer pays. Supply chain finance works from the other side: the buyer’s bank pays the supplier early on the strength of the buyer’s credit rating, which can mean cheaper funding for a smaller supplier than it could arrange alone.

| Where the gap hurts | Tool that fits | What it does |

| Customers pay slowly | Invoice finance / factoring | Advances cash against receivables |

| Capital tied up in kit | Asset finance / ABL | Releases cash against assets |

| Big order, no cash to start | Production / PO finance | Funds the order, repaid on sale |

| Buyer wants long terms | Supply chain finance | Buyer’s bank pays supplier early |

Closing the gap

Finance is half the answer; discipline is the other half. The strongest manufacturers shorten the gap from both ends. They forecast cash, not just profit, so a shortfall is visible weeks ahead rather than on the day it bites. They negotiate terms in both directions — a deposit from the customer, a little longer to pay a supplier — to pull the two halves of the cycle closer together. And they match the financing tool to the actual problem rather than reaching for whatever is nearest, because invoice finance won’t fix an equipment bottleneck and a term loan won’t cure slow payers. The aim isn’t to borrow more; it’s to make the timing survivable.

Bottom line

A manufacturer’s profit and loss account and its bank statement tell two different stories, and it’s the bank statement that decides whether the doors stay open. The cash flow gap is structural — money goes out to make things long before it comes back from selling them — and growth widens it rather than closing it. The businesses that endure are the ones that treat cash flow as seriously as their order book: forecasting it, negotiating around it, and using the right finance to bridge the stretch between paying and being paid. Profit is the goal. Cash is the oxygen.