Storm Eunice fails to dampen footfall

Covering the four weeks 30 January – 26 February 2022

Since the pandemic started, much of retail has bounced between being open and closed, impacting footfall significantly. To make meaningful comparisons to changes in footfall, all figures since March 2021 are compared to their pre-pandemic levels (year-on-2-years, Yo2Y), rather than year-on-year.

According to BRC-Sensormatic IQ data:

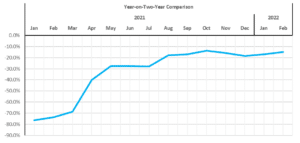

- Total UK footfall decreased by 14.9% in February (Yo2Y), a 2.2 percentage point improvement from January. This is better than the 3-month average decline of 17.2%.

- This was ahead of Spain (-16.4%), France (-20.3%), Italy (-29.1%) and Germany (-42.6%) in February (Yo2Y).

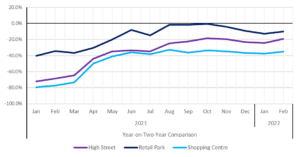

- Footfall on High Streets declined by 19.4% in February (Yo2Y), 4.8 percentage points better than last month’s rate, and an improvement on the 3-month average decline of 22.4%.

- Retail Parks saw footfall decrease by 10.2% (Yo2Y), 2.8 percentage points better than last month’s rate, and an improvement on the 3-month average decline of 10.7%.

- Shopping Centre footfall declined by 35.2% (Yo2Y), 2.3 percentage points better than last month’s rate, and an improvement on the 3-month average decline of 36.8%.

- England saw the shallowest footfall decline of all regions at -14.4%, followed by Northern Ireland at -15.5% and Wales at -17.1%. Scotland saw the steepest decline at -17.5%.

Helen Dickinson OBE, chief-executive of British Retail Consortium, said: “UK footfall led the major European economies in February, as the steady return to the office increased shopper numbers in many towns and city centres. A promising start to the month was briefly dampened by Storm Eunice, before bouncing back in the final week of February, to its highest level since the pandemic began. This coincided with the easing of Covid restrictions in England. Overall, the major cities enjoyed the biggest improvements, particularly London, Manchester, and Birmingham.

“Retailers, large and small, will welcome the return of customers to their stores – a sign their innovation and investment in their physical and digital offerings is working. However, challenges remain; consumer confidence has been greatly impacted by rising inflation, while the return of hospitality and tourism will create additional competition. Retailers will need to continue the momentum to keep consumers engaged.”

Andy Sumpter, retail consultant EMEA for Sensormatic Solutions, commented: “February saw an improving picture for the High Street as shopper traffic continued to recover. Total UK footfall reported the highest number of shopper counts seen since pre-pandemic levels in the last week of the month and the UK now leads the top 5 European markets’ footfall recovery, suggesting a growing confidence among shoppers, with UK Governments announcing the further easing and ending of covid restrictions. And while this represents what many, not least retailers, hope will be the ‘beginning of the end’ of the covid crisis – our latest data shows consumer concern about in-store safety fell by -18 percentage points year-on-year – shoppers now face new and growing pressures. The cost-of-living squeeze and inflation, which is putting downward pressures on disposable income, and a volatile macroeconomic and geopolitical climate could create a perfect storm of uncertainty for consumers, which could still impact the long-term retail recovery as it looks to build back post-pandemic.”

MONTHLY TOTAL UK RETAIL FOOTFALL (% CHANGE Yo2Y)

UK FOOTFALL BY LOCATION (% CHANGE Yo2Y)

TOTAL FOOTFALL BY REGION (% CHANGE Yo2Y)

| GROWTH RANK | REGION | % GROWTH Yo2Y |

| 1 | North West England | -7.9 |

| 2 | Yorkshire and the Humber | -10.1 |

| 3 | West Midlands | -11.0 |

| 4 | East of England | -12.2 |

| 5 | South West England | -12.7 |

| 6 | East Midlands | -13.3 |

| 7 | North East England | -13.3 |

| 8 | South East England | -13.7 |

| 9 | England | -14.4 |

| 10 | Northern Ireland | -15.5 |

| 11 | Wales | -17.1 |

| 12 | Scotland | -17.5 |

| 13 | London | -22.7 |

TOTAL FOOTFALL BY CITY (% CHANGE Yo2Y)

| GROWTH RANK | CITY | % GROWTH Yo2Y |

| 1 | Manchester | -3.0 |

| 2 | Portsmouth | -4.5 |

| 3 | Liverpool | -7.2 |

| 4 | Leeds | -13.7 |

| 5 | Bristol | -13.9 |

| 6 | Nottingham | -14.4 |

| 7 | Birmingham | -14.6 |

| 8 | Cardiff | -17.0 |

| 9 | Belfast | -17.8 |

| 10 | Glasgow | -19.0 |

| 11 | London | -21.9 |