The rise of BNPL in Asia-Pacific: Opportunities for financial institutions

The Buy Now, Pay Later (BNPL) model has rapidly transformed from a niche offering into a mainstream financial product across Asia-Pacific. This payment solution has redefined how consumers finance purchases, providing a flexible alternative to traditional credit cards and bank loans. With the global BNPL market valued at US$6.13 billion, the Asia-Pacific region alone contributes a staggering US$120 billion in 2023, making it the largest BNPL market worldwide. For financial institutions, this growth presents an exciting opportunity to explore the unique consumer demand in the region and carve out a competitive position in this burgeoning sector. This article delves into the key drivers behind the BNPL surge in Asia-Pacific and outlines the opportunities it presents for banks and financial institutions.

1. The BNPL boom in Asia-Pacific

Asia-Pacific’s BNPL market has expanded rapidly in recent years, driven by factors such as e-commerce growth, increased smartphone penetration, and a younger population open to alternative finance solutions. As more consumers turn to BNPL to manage expenses, the region is leading the way in the BNPL revolution. Unlike in other markets where BNPL is still gaining traction, Asia-Pacific has a highly receptive consumer base. This enthusiastic adoption creates a massive opportunity for financial institutions to develop tailored BNPL solutions or collaborate with established BNPL providers to reach these tech-savvy consumers.

The projected growth of the BNPL market in Singapore, where users are expected to rise from 1.9 million in 2022 to 3.7 million by 2032, exemplifies the market’s potential. Singapore serves as a microcosm for Asia-Pacific’s BNPL landscape, showcasing a tech-savvy consumer base with a strong appetite for digital financial solutions. Banks and other financial entities can leverage this interest by creating strategic BNPL offerings to capture market share early.

2. Why consumers are embracing BNPL

Consumer motivations behind BNPL adoption in Asia-Pacific are varied, yet three primary factors stand out: zero-interest credit (36%), flexible payment terms (17%), and rewards like discounts and cashback (16%). These features make BNPL a more attractive option than traditional credit products, especially for younger consumers looking to avoid the high-interest rates associated with credit cards. For banks, this presents an opportunity to attract younger demographics by offering similar or enhanced benefits within their own BNPL models.

Moreover, the demand for flexible payment options signals a shift in consumer behavior, where budgeting and control over spending have become more critical. By incorporating these preferences into their products, financial institutions can develop BNPL services that not only meet current demand but also drive customer loyalty in the long term.

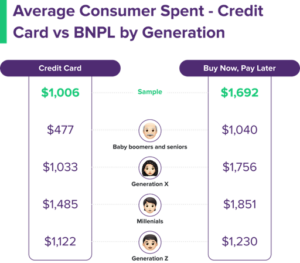

3. Generational shifts in spending: BNPL vs. traditional credit

Younger consumers, particularly Millennials and Generation Z, are favoring BNPL over credit cards for specific spending needs. Recent data reveals that Millennials spend an average of US$1,851 through BNPL services, compared to US$1,485 with credit cards. Generation Z follows a similar trend, with an average BNPL spend of US$1,230 versus US$1,122 on credit cards. The flexibility and control BNPL offers are particularly appealing to these generations, as they enable budgeting without the burden of revolving debt. Financial institutions can tap into this trend by targeting younger consumers with BNPL options that align with their spending habits and values.

Additionally, the shift towards BNPL can be attributed to the perceived transparency and ease of use compared to traditional credit. For banks and financial institutions, adapting to these generational shifts by offering BNPL products will allow them to compete effectively in a market increasingly driven by alternative payment options.

4. Opportunities for financial institutions in the BNPL space

The demand for BNPL provides financial institutions with numerous opportunities to diversify their offerings and attract new customers. They can enter the market through three primary approaches:

- In-house BNPL offerings: Banks can develop their own BNPL services, integrating them within existing banking apps to provide a seamless experience for customers.

- Partnerships with existing BNPL providers: Collaborating with established BNPL companies allows banks to enter the market quickly and benefit from existing technology and customer bases.

- Co-branded BNPL products: Co-branded offerings enable banks to build brand loyalty while leveraging the established BNPL infrastructure of their partners.

The strategic move into BNPL can offer financial institutions access to new revenue streams and enhance customer engagement. By capitalizing on the rapid adoption of BNPL in Asia-Pacific, banks can strengthen their relevance in a digital-first market and create long-lasting relationships with a younger, tech-savvy demographic.

5. Key drivers for consumer satisfaction

Understanding the primary drivers behind BNPL satisfaction is crucial for financial institutions aiming to create a compelling BNPL offering. The key factors that contribute to positive user experiences include a straightforward application process (67%), a quick approval process (50%), and transparency around fees and surcharges (39%). Financial institutions can prioritize these features to enhance user satisfaction and differentiate their offerings in a competitive market.

By ensuring that BNPL services are transparent, easy to use, and quick to approve, banks can build consumer trust and foster loyalty. Such strategies are essential for long-term success in the BNPL market, where customer satisfaction and retention play pivotal roles in growth.

6. The global BNPL market and key segments

The global BNPL market is segmented across online and retail channels, with over 65% revenue coming from online channels and 73% from retail. This segmentation underscores the versatility of BNPL across different sectors, making it a lucrative option for banks looking to diversify their portfolios. Asia-Pacific’s large share of the BNPL market highlights the region’s role as a testing ground for innovative BNPL solutions, offering financial institutions insights into consumer behavior and spending patterns in a high-growth environment.

As banks look to expand their digital finance offerings, understanding the strengths of BNPL in online and retail sectors can help them tailor their solutions. Financial institutions that strategically position themselves in the BNPL market can not only enhance customer engagement but also strengthen partnerships with retailers, adding further value to their product offerings.

7. Challenges and considerations for financial institutions

While BNPL presents promising opportunities, it also comes with challenges. Financial institutions must navigate regulatory scrutiny to ensure responsible lending practices and mitigate the risk of consumer overextension. As BNPL services become increasingly popular, regulators are focusing on transparency, data privacy, and the potential financial risks associated with BNPL. Banks and fintech companies must therefore maintain high standards of transparency and align with local regulatory requirements.

Another challenge is competing with established BNPL providers that already dominate the market. For financial institutions entering the BNPL space, differentiation is key. Offering superior customer experiences, transparent terms, and streamlined processes can set new entrants apart and encourage customer loyalty in a market where competition is fierce.

Conclusion: Unlocking the potential of BNPL in Asia-Pacific

The rise of BNPL in Asia-Pacific marks a transformative shift in consumer finance, offering banks and financial institutions a unique opportunity to diversify their product portfolios and meet the evolving needs of a digital-first population. By understanding the factors driving BNPL adoption and focusing on transparency, ease of use, and competitive repayment terms, financial institutions can capture a share of this growing market.

As BNPL reshapes the financial landscape in Asia-Pacific, proactive institutions will be well-positioned to lead in this fast-growing segment. By investing in BNPL offerings or partnerships, banks can enhance their relevance, attract new customers, and foster long-term growth in a region that is setting the pace for global digital finance innovation.

This article is brought to you by ROSHI, the ultimate platform for all fast cash loan needs in Singapore. With advanced technology and a team of experienced loan specialists, ROSHI connects users with the ideal loan options directly on their platform, streamlining the application process and expediting approval. Whether it’s from licensed moneylenders, home financing, or they want to know where to borrow money in Singapore, ROSHI simplifies the journey to finding the perfect loan.