Trust management strategies military families should understand before retirement

Military families often deal with financial situations that civilian households never face. Frequent moves, deployment schedules, changing state residency rules, survivor benefits, pensions, and long-term care planning can all affect how money is handled over time. Many service members spend years focused on their careers and family responsibilities while putting estate planning on the back burner. The problem is that trust management works best when it is set up before a crisis happens. A well-built trust can help reduce confusion, protect children, simplify asset transfers, and make life easier for surviving family members during difficult moments.

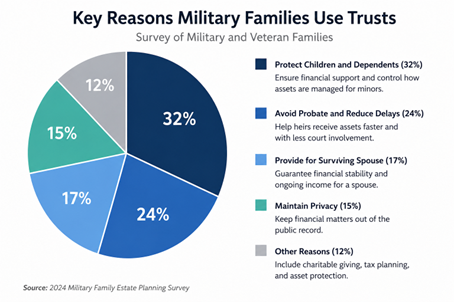

Why trusts matter

Trusts are not reserved for wealthy retirees with vacation homes and giant investment portfolios. Many middle-class military households can benefit from them because military life often creates more legal complexity than civilian life. Families may own property in different states, maintain military benefits, or relocate often enough that probate issues become messy later.

A revocable living trust gives the creator control over assets during their lifetime while helping family members avoid a lengthy probate process after death. Military spouses may especially benefit from having organized instructions already in place if sudden deployments, illness, or emergencies occur.

Trusts can also help blended families manage inheritance decisions more clearly. Without one, disagreements can happen after someone passes away, especially when adult children, stepchildren, or multiple marriages are involved.

Building long-term stability

Financial planning has become a larger focus for military households over the past decade. More families are preparing for retirement earlier, creating businesses after service, and thinking beyond traditional pension income. Discussions around veterans becoming entrepreneurs have also pushed many military families to think more seriously about asset protection and long-term financial organization.

A trust can help protect a business interest, rental property, or investment account while also establishing instructions for future generations. Parents often use trusts to control how younger beneficiaries receive money instead of handing over large sums at once. Some families choose age-based distributions while others structure funds around education, housing, or medical expenses.

Military pensions and survivor benefits should also be reviewed alongside trust planning. A trust does not replace beneficiary designations, but it can work together with them to create a more organized estate strategy. Families who fail to coordinate these areas sometimes leave surviving spouses dealing with avoidable legal and financial confusion.

Choosing professional guidance

Military benefits and retirement systems are different from civilian financial structures. That is why many households seek advisors who understand military-specific planning concerns. Financial professionals who regularly work with military families often understand deployment pay, VA-related income considerations, survivor benefits, and military pension structures more thoroughly than a general advisor.

Many families specifically seek out firms that specialize in military wealth management because they want guidance tailored to the realities of service life. This can include planning around relocation, tax considerations in multiple states, trust structures for children, and strategies for retirement transitions after active duty.

Not every financial advisor handles trust planning directly. Some work alongside estate attorneys to create a complete strategy. Military families should look for professionals who communicate clearly and explain legal structures in plain language instead of drowning clients in jargon. If an advisor cannot explain a trust in understandable terms, that usually becomes a problem later when family members actually need to use the documents.

Protecting children and spouses

One of the biggest reasons military families establish trusts is to protect children if something unexpected happens. A trust can determine how money is managed for minors and who controls those funds until children reach a certain age. Without that structure, courts may become more involved in managing inherited assets.

Spouses can also benefit from trust protections. Some trusts are designed to provide income to a surviving spouse while preserving assets for children later. Others help ensure that family property remains protected if a surviving spouse remarries or faces financial hardship.

Military life can already place emotional stress on families. Clear legal planning removes uncertainty during emergencies. Many people assume estate planning is mostly about money, but in reality it is often about reducing chaos during painful situations. Families who organize these decisions early usually leave fewer burdens behind for loved ones.

Updating plans regularly

Creating a trust once and forgetting about it is a common mistake. Military families experience major life changes more frequently than many civilians. Relocations, career changes, deployments, marriages, divorces, births, and retirements can all affect estate planning needs.

A trust should be reviewed every few years or after major family changes. Beneficiary designations on retirement accounts and insurance policies should also match the broader estate plan. If those documents conflict, problems can arise even when the trust itself is well written.

Retirement is another important checkpoint. Some military retirees transition into civilian careers, consulting work, or business ownership after leaving active duty. Others downsize, relocate, or begin helping adult children financially. These changes can alter how assets should be structured and protected.

Families should also make sure trustees know where important documents are stored. A beautifully written trust does little good if nobody can locate it when needed.

Avoiding common mistakes

One common mistake is assuming a trust automatically controls every asset. In reality, assets usually need to be properly titled into the trust for it to work as intended. Another mistake is relying entirely on online templates without legal review. Generic forms may overlook military-specific concerns or state-level legal requirements.

Some families also wait too long because estate planning feels uncomfortable. Nobody enjoys discussing death, illness, or incapacity. Still, delaying important decisions rarely makes those realities easier later.

Trust management works best when families view it as part of overall financial readiness. Military households already understand preparation better than most people. Estate planning follows the same basic principle. The more organized the plan, the less uncertainty loved ones face later.

Trust management gives military families more control, structure, and protection during major life transitions. A strong plan can help preserve stability for spouses, children, and future generations while reducing unnecessary stress during difficult moments.