Why cash flow is king and profit is queen

Defining the royal pair: The fundamentals of profit and cash flow

In the complex world of business finance, profit and cash flow are two terms often used interchangeably. But for any business to truly thrive, understanding their distinct roles is paramount. Think of it this way: if your business were a kingdom, cash flow would be the powerful king, ensuring daily operations run smoothly and bills are paid. Profit, on the other hand, would be the wise queen, signaling long-term prosperity and overall wealth.

In the complex world of business finance, profit and cash flow are two terms often used interchangeably. But for any business to truly thrive, understanding their distinct roles is paramount. Think of it this way: if your business were a kingdom, cash flow would be the powerful king, ensuring daily operations run smoothly and bills are paid. Profit, on the other hand, would be the wise queen, signaling long-term prosperity and overall wealth.

Many businesses, despite showing healthy profits on paper, can crumble due to a lack of immediate cash. Conversely, a company with plenty of cash might still be on a path to ruin if it consistently fails to generate profit.

We will dig into the fundamental definitions of profit and cash flow. We will explore their key differences, how they relate to each other, and why a holistic view of both is vital for any business owner. Join us as we explain these critical concepts and show you how to ensure both the king and queen are thriving in your financial kingdom.

The financial health of a business is often assessed through its key financial statements: the Income Statement (also known as the Profit and Loss, or P&L statement) and the Cash Flow Statement. These documents, built upon the principles of accrual accounting, offer distinct yet complementary insights into a company’s performance and stability. Understanding them is the first step in mastering the dynamics of our financial kingdom.

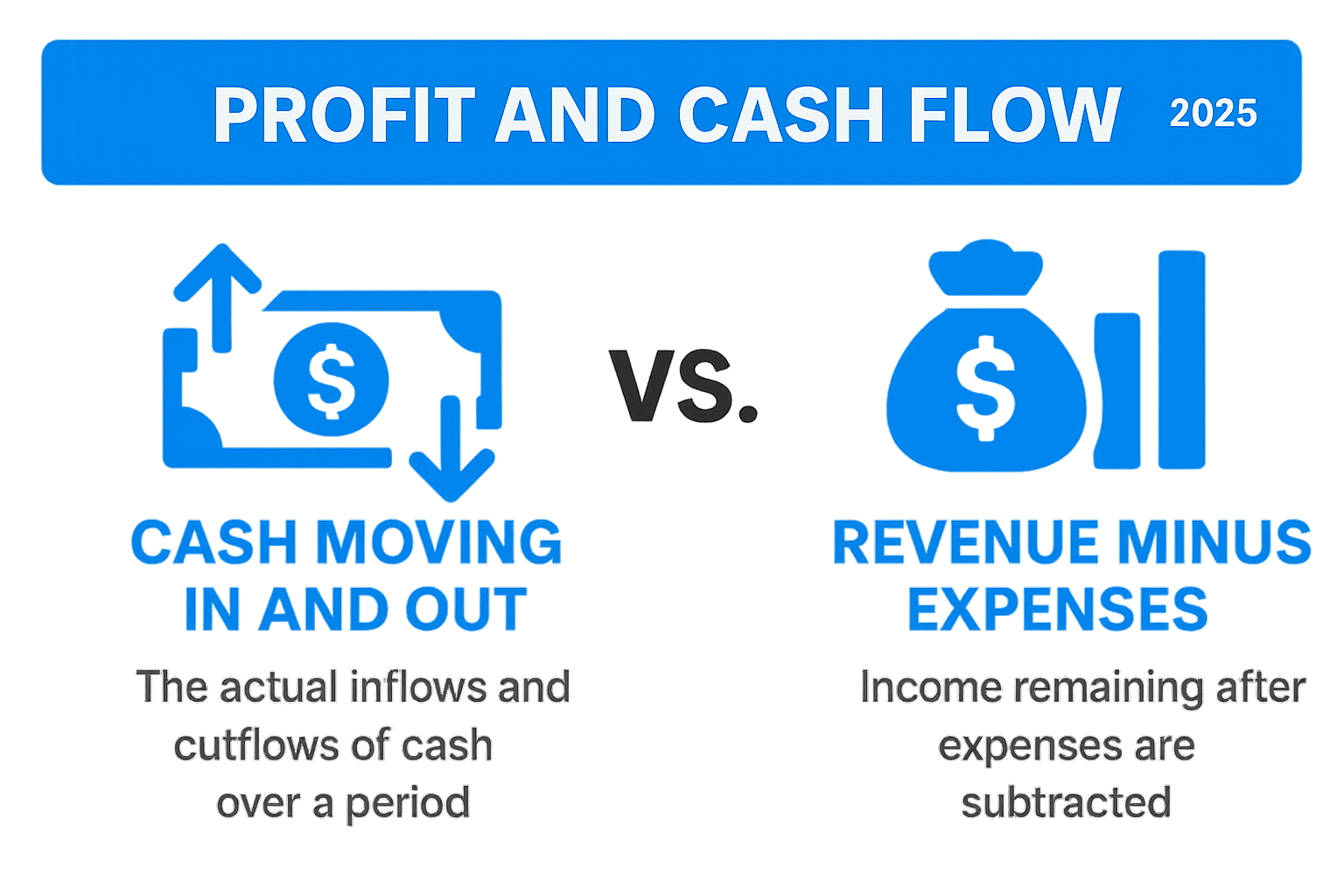

Profit: The measure of long-term prosperity (the queen)

What is profit? At its core, profit represents the financial gain a business achieves after deducting all its expenses from its revenues over a specific period. It is the “bottom line” on the Income Statement, indicating whether a company is generating wealth from its operations. Profit is also widely known as net income.

How is profit calculated? The journey to net profit involves several stages, each providing a different perspective on a company’s profitability:

- Gross profit: This is the first level of profit, calculated by subtracting the Cost of Goods Sold (COGS) from your total revenue. COGS includes the direct costs attributable to the production of the goods or services sold by a company. For example, if you sell a product for $10 and it cost you $4 to produce, your gross profit is $6. This metric shows how efficiently a business produces its goods or services.

- Operating profit (or EBIT – earnings before interest and taxes): Taking gross profit a step further, operating profit is calculated by subtracting all operating expenses (such as salaries, rent, marketing, and utilities) from gross profit. This figure reveals the profitability of a company’s core operations, before considering interest payments on debt or taxes. It highlights the efficiency of management in controlling day-to-day business costs.

- Net profit (or net income): This is the ultimate measure of a company’s profitability, often referred to as “the bottom line.” Net profit is derived by deducting all remaining expenses, including interest expenses and income taxes, from the operating profit. It represents the total earnings available to shareholders or for reinvestment into the business.

Profit is crucial because it indicates the long-term viability and growth potential of a business. A company consistently making profits is generally considered healthy and sustainable. However, as we will explore, a business can operate without seeing profits for a period, especially during growth phases or in startups, as long as other financial aspects are managed effectively.

Cash flow: The lifeblood of daily operations (the king)

What is cash flow? Cash flow, in contrast to profit, refers to the actual movement of money into and out of your business over a specific period. It’s about liquidity – whether you have enough physical cash (or cash equivalents) to cover your immediate obligations. Positive cash flow means more money is coming in than going out, while negative cash flow indicates the opposite. Cash flow is reported on the Cash Flow Statement, a critical financial document that tracks every dollar.

How is cash flow calculated? The Cash Flow Statement categorizes cash movements into three main types of activities, providing a comprehensive picture of where a company’s cash is coming from and where it’s going:

- Cash flow from operating activities (CFO): This is the cash generated or used by a company’s normal, day-to-day business operations. It includes cash received from customers for sales and cash paid for operating expenses like salaries, rent, and supplier payments. Often called the “lifeblood” of an organization, positive operating cash flow indicates that a business can generate enough cash from its primary activities to sustain itself.

- Cash flow from investing activities (CFI): This section reflects cash used for or generated from the purchase or sale of long-term assets, such as property, plant, and equipment (PP&E), or investments in other companies. A healthy, growing company often shows negative cash flow from investing activities as it pours money into expanding its asset base.

- Cash flow from financing activities (CFF): This category includes cash transactions related to debt, equity, and dividends. It covers cash received from issuing new debt or equity, and cash paid for debt repayments, share repurchases, or dividend distributions to shareholders.

Understanding cash flow is paramount because, regardless of how profitable a business appears on paper, it needs sufficient cash to pay its bills, employees, and suppliers. A lack of cash, even for a profitable business, can lead to insolvency.

The royal court’s dynamics: Key differences and interplay

The most significant distinction between profit and cash flow stems from their underlying accounting principles. Profit is largely governed by accrual accounting, while cash flow, by definition, tracks actual cash movements. This fundamental difference creates scenarios where the queen (profit) might appear robust, yet the king (cash) is struggling, or vice versa.

Why profit isn’t cash: The accrual accounting divide

Accrual accounting is the standard method for preparing financial statements. It dictates that revenues are recognized when they are earned, and expenses are recognized when they are incurred, regardless of when cash actually changes hands. This provides a more accurate picture of a company’s financial performance over a period, adhering to the “matching principle” where expenses are matched with the revenues they helped generate.

However, this also means that profit can include “non-cash” items or be affected by timing differences that don’t immediately impact cash:

- Credit sales (accounts receivable): When a business makes a sale on credit, it recognizes the revenue immediately on its Income Statement, boosting profit. However, the actual cash inflow doesn’t occur until the customer pays the invoice, which could be 30, 60, or even 90 days later. This can lead to a situation where a company is profitable on paper but has negative cash flow because its cash is tied up in outstanding receivables.

- Non-cash expenses (depreciation and amortization): These are expenses that reduce a company’s profit but do not involve an actual outflow of cash. Depreciation, for example, allocates the cost of a long-lived asset (like machinery or a building) over its useful life. While it reduces net profit on the Income Statement, it’s simply an accounting entry and doesn’t represent a cash payment in the current period. Therefore, when calculating cash flow from operations using the indirect method, depreciation is typically added back to net income.

- Inventory purchases: A business might purchase a large amount of inventory, leading to a significant cash outflow. However, the cost of that inventory (COGS) is only recognized on the Income Statement when the goods are actually sold. This can create a temporary cash shortage even if sales are strong.

- Prepaid expenses: If a company pays for an expense in advance (e.g., a year’s worth of insurance), the full cash outflow occurs upfront. However, under accrual accounting, the expense is recognized gradually over the period it covers, impacting profit incrementally.

To illustrate the difference, consider a simple transaction:

Scenario: A company sells a product for $1,000 on credit. Income Statement (Accrual Basis)Cash Flow Statement (Cash Basis Revenue: $1,000 (recognized immediately) Cash from Operations: $0 (until payment is received) Cost of Goods Sold: $X Profit: $1,000 – $X This table clearly shows how profit can be recognized without any immediate cash changing hands, highlighting the crucial timing difference that accrual accounting introduces.

Can the kingdom thrive with only one ruler?

The interplay between profit and cash flow is complex, and a healthy business needs both. However, it’s entirely possible for one to be strong while the other is weak, leading to distinct challenges:

- Profitable with negative cash flow: This is a common and often dangerous scenario, especially for rapidly growing businesses. A company might be selling a lot of products, recognizing significant revenue, and showing a healthy net profit. However, if customers are paying slowly (high accounts receivable), or if the company is investing heavily in new inventory or capital expenditures (like new equipment), it can quickly run out of cash. This is sometimes referred to as a “growth trap,” where increased sales paradoxically create cash flow problems because cash is tied up before it can be collected. Such a business, despite its profitability on paper, might struggle to pay its employees, suppliers, or even its taxes, potentially leading to bankruptcy. For example, it’s possible for a company to be both profitable and have a negative cash flow hindering its ability to pay its expenses, expand, and grow.

- Positive cash flow with no profit: Conversely, a business can have plenty of cash but still be unprofitable. This often happens with startups or scaling businesses that receive significant upfront investments (positive cash flow from financing activities) or collect cash quickly (e.g., subscription models, retail sales). However, if their expenses (marketing, R&D, salaries) consistently outweigh their revenues, they will be burning through their cash reserves without generating sustainable earnings. While they may have positive cash flow and increasing sales, they fail to make a profit. While cash is flowing in, the underlying business model may not be viable in the long run. Investors, particularly during economic downturns, might prioritize cash flow over current profitability due to its indication of future resilience, but long-term profitability is essential for survival.

Neither cash flow nor profit is singularly more important; a holistic view using multiple financial statements is necessary for understanding a business’s situation.

Understanding free cash flow vs. net profit

While net profit is the ultimate measure of a company’s accounting profitability, Free Cash Flow (FCF) offers a different, often more telling, perspective for investors and analysts. FCF represents the cash a company has left over after paying its operating expenses and capital expenditures (CapEx). This is the cash available to distribute to creditors and shareholders, or to reinvest in non-core growth opportunities.

FCF is generally considered a more accurate indicator of a company’s financial health and value than net profit because it is less susceptible to accounting manipulations and non-cash items. Unlike net profit, which can be inflated by aggressive revenue recognition or reduced by non-cash expenses, FCF directly measures the cash available for discretionary use. It specifically accounts for the cash outflows related to maintaining and expanding the business’s asset base (CapEx), which net profit does not. For example, Free Cash Flow = Net Income + Depreciation/Amortization – Change in Working Capital – Capital Expenditure. This makes FCF a powerful metric for assessing a company’s ability to generate cash internally, pay down debt, fund growth, or return money to shareholders.

A guide to effective financial governance

Effective financial governance means striking a delicate balance between the King (cash flow) and the Queen (profit). Prioritizing one over the other can lead to significant problems. For instance, focusing solely on profit without managing cash flow can result in a profitable business collapsing due to a lack of liquidity. Conversely, generating cash at any cost, perhaps by slashing prices too aggressively, might boost cash flow temporarily but erode profit margins, making the business unsustainable in the long run.

Strategies for managing cash flow effectively

Given that cash is the immediate lifeblood of any business, effective cash flow management is paramount. Here are key strategies to ensure your King remains strong, especially during periods of growth or economic downturn:

- Cash flow forecasting: This is perhaps the most critical tool. By accurately projecting your cash inflows and outflows for future periods (weekly, monthly, quarterly), you can anticipate potential shortfalls or surpluses. This proactive approach allows you to make informed decisions, such as delaying non-essential purchases or seeking short-term financing, before a crisis hits.

- Managing accounts receivable: Speed up your cash inflows by invoicing customers immediately and following up diligently on overdue payments. Consider offering early payment discounts (e.g., 2-5% off for payment within 3-10 days) or implementing stricter credit policies for new customers. The faster you collect, the healthier your cash position.

- Negotiating accounts payable: While you want to pay your suppliers on time to maintain good relationships, strategically negotiating longer payment terms (e.g., 60 days instead of 30) can help you preserve cash longer. Balance this with the potential for early payment discounts from suppliers.

- Inventory control: For businesses that deal with physical products, inventory can be a significant drain on cash. Optimize your inventory levels to avoid tying up excessive capital in unsold goods. Implement just-in-time (JIT) inventory practices where feasible to reduce holding costs and free up cash.

- Maintaining a cash reserve: Just like a personal emergency fund, a business should aim to keep a buffer of cash readily available to cover unexpected expenses or revenue dips. This liquid reserve provides financial stability and peace of mind.

- Controlling expenses: Regularly review all operating expenses to identify areas where costs can be reduced without negatively impacting quality or customer service. This might involve renegotiating contracts, finding more efficient suppliers, or optimizing energy consumption.

Balancing the books to achieve healthy profit and cash flow

Investors and lenders carefully scrutinize both profit and cash flow when evaluating a business. While profit indicates a company’s long-term earning potential, cash flow demonstrates its ability to meet immediate obligations and fund future growth without relying solely on external financing.

- Investor perspective: Investors look for a track record of both profitability and strong cash flow. A profitable company with consistent positive cash flow is attractive because it indicates financial stability and the ability to generate returns. During economic downturns, investors might especially prioritize cash flow, as it signals a company’s resilience and ability to weather financial storms. They understand that increased sales can create cash flow problems if not managed carefully.

- Lender evaluation: When a business seeks a loan, lenders assess its capacity to repay. While net profit is a starting point, they often adjust it by adding back non-cash expenses like depreciation to get a clearer picture of the cash available for debt service. This is because depreciation reduces profit on paper but doesn’t require a cash outlay. Lenders want to see robust cash flow from operations, as this is the primary source for loan repayments.

The goal is to achieve a holistic financial strategy where both the King and Queen flourish. This means making strategic decisions that support both liquidity and long-term profitability. It involves understanding that while a business can be profitable on paper and have negative cash flow, or have positive cash flow and fail to make a profit, neither scenario is sustainable indefinitely. For a deeper dive into creating a robust financial strategy, consider resources that help you optimize your business’s profit and cash flow.

Frequently asked questions about profit and cash flow

The nuances between profit and cash flow often lead to common questions. Let’s address some of these to solidify our understanding of these vital financial metrics.

Which is more important, profit or cash flow?

This is a frequently asked question, and the answer is: neither is inherently “more important” than the other; both are crucial for a business’s health and survival, but they serve different purposes and their relative importance can shift based on the business’s current stage and circumstances.

- For short-term survival, cash flow is king. A business can be profitable on paper but still go bankrupt if it runs out of cash to pay its immediate bills (payroll, suppliers, rent). Cash flow ensures liquidity and the ability to operate day-to-day.

- For long-term viability and growth, profit is queen. Consistent profitability indicates that your business model is sound, that you are generating more revenue than expenses, and that you are creating wealth. Without profit, a business cannot sustain itself indefinitely, reinvest in its future, or attract long-term investors.

A financially healthy business needs both positive cash flow and consistent profitability. They are two sides of the same coin, each providing unique insights into the overall financial picture. A holistic view using multiple financial statements is necessary to truly understand the business’s situation.

Can a business be profitable but have negative cash flow?

Yes, absolutely. This is a very common scenario, especially for fast-growing businesses. As discussed earlier, this often happens due to:

- Rapid growth: Increased sales often mean increased production, which requires upfront cash for raw materials, inventory, and labor, long before the cash from those sales is collected.

- High accounts receivable: If a business sells a lot on credit and its customers take a long time to pay, profit will be high, but cash will be low.

- Large inventory purchases: Buying a significant amount of inventory to meet future demand ties up cash, even if those goods haven’t been sold yet.

- Significant capital investments: Investing in new machinery, technology, or expanding facilities requires substantial cash outflows, which reduce cash flow from investing activities but are expensed over time (depreciation) on the income statement.

In these situations, the business is making money (profitable), but it doesn’t have enough liquid funds to cover its immediate obligations. This is why understanding both metrics is so critical.

How does depreciation affect profit and cash flow?

Depreciation is a prime example of a non-cash expense that highlights the difference between profit and cash flow.

- Impact on profit: Depreciation is recorded on the Income Statement as an expense. It systematically allocates the cost of a tangible asset over its useful life. By including depreciation, a business’s taxable income and net profit are reduced. This is a good thing for tax purposes, as it lowers the amount of tax owed.

- Impact on cash flow: However, depreciation does not involve an actual outflow of cash in the period it is recorded (the cash outflow occurred when the asset was initially purchased). Therefore, when calculating cash flow from operating activities using the indirect method, depreciation is added back to net income. This adjustment removes the non-cash effect of depreciation, allowing the statement to reflect the true cash generated from operations.

Depreciation reduces profit but does not directly affect cash flow in the current period, making it a key reason why net profit and cash flow often diverge.

Conclusion

In the intricate dance of business finance, both cash flow (the king) and profit (the queen) play indispensable roles. Cash flow ensures the daily survival and operational fluidity of your business, providing the immediate resources needed to meet obligations and seize opportunities. Profit, on the other hand, is the ultimate indicator of your business’s long-term health, sustainability, and ability to generate wealth.

Understanding their distinct definitions, calculation methods, and the dynamic interplay between them is not just an academic exercise; it is fundamental to effective financial management. A business cannot thrive indefinitely with only one ruler. A profitable business without sufficient cash flow risks insolvency, while a cash-rich business that consistently fails to generate profit is ultimately unsustainable.

By diligently monitoring both your Income Statement and Cash Flow Statement, understanding the impact of accrual accounting, and proactively managing your financial resources, you empower your business to achieve true financial stability and sustainable growth. Ensure both your King and Queen are strong, and your financial kingdom will prosper.